NPS Tier II Withdrawal Tax Rules: A Comprehensive Guide for Indian Investors

As retirement planning gains momentum across India's salaried and self-employed workforce, the National Pension System (NPS) has emerged as one of the most versatile long-term investment vehicles available. While Tier I accounts attract significant attention for their tax-saving benefits, the NPS Tier II withdrawal tax rules remain poorly understood — even among seasoned investors and banking professionals. A recent tax query circulating in financial forums — "Is withdrawal from NPS Tier II equity fund taxable as LTCG?" — underscores just how much confusion exists around this subject. This article cuts through the ambiguity, providing a definitive, structured analysis of how NPS Tier II withdrawals are taxed in India, what asset class distinctions matter, and what mistakes you must avoid when planning your exit strategy.

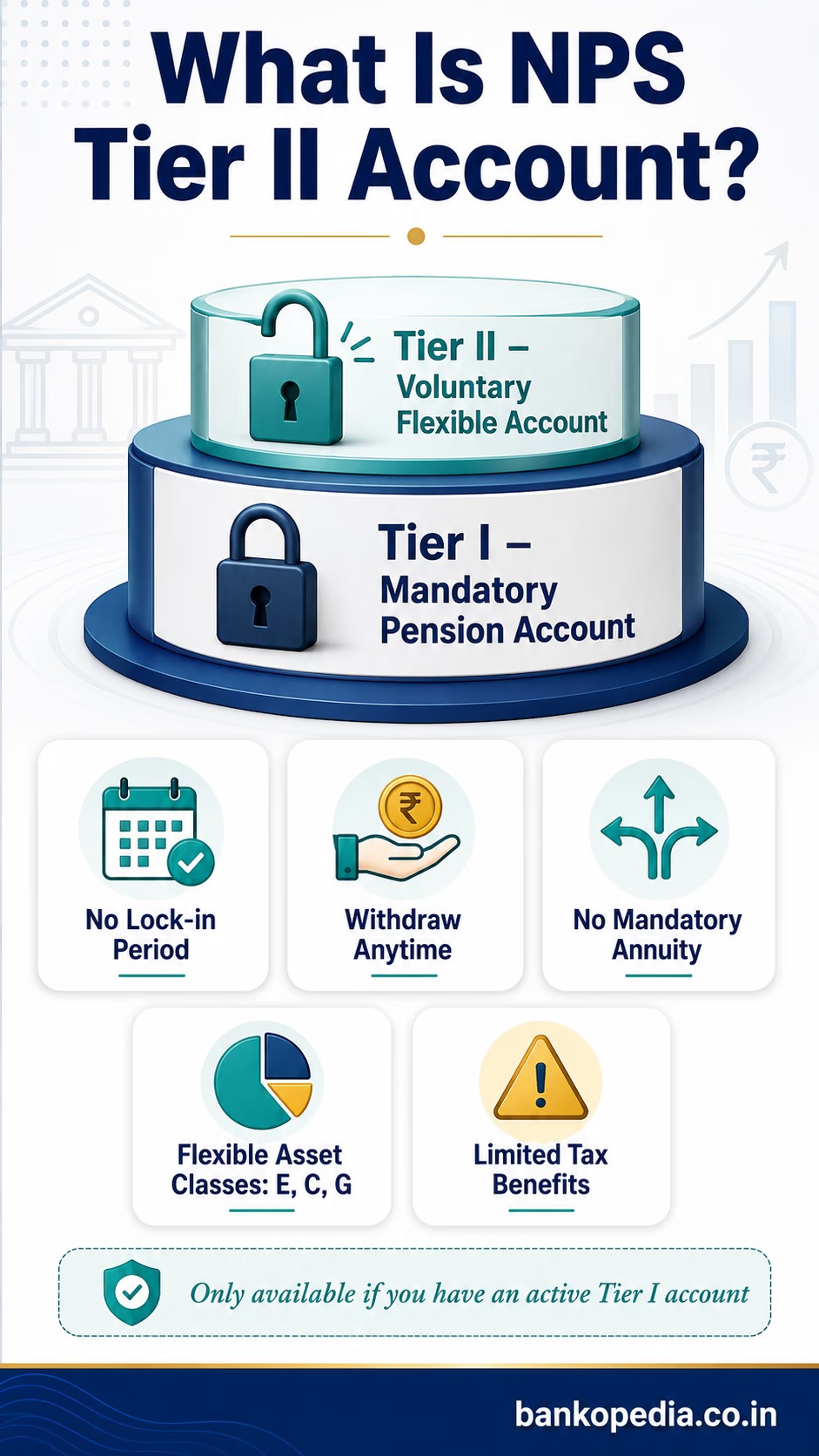

What Is NPS Tier II Account and How Does It Differ from Tier I?

The National Pension System, regulated by the Pension Fund Regulatory and Development Authority (PFRDA), offers subscribers two account types: Tier I and Tier II. Understanding their structural differences is essential before examining their tax treatment.

NPS Tier I: The Pension-Cum-Tax-Saving Account

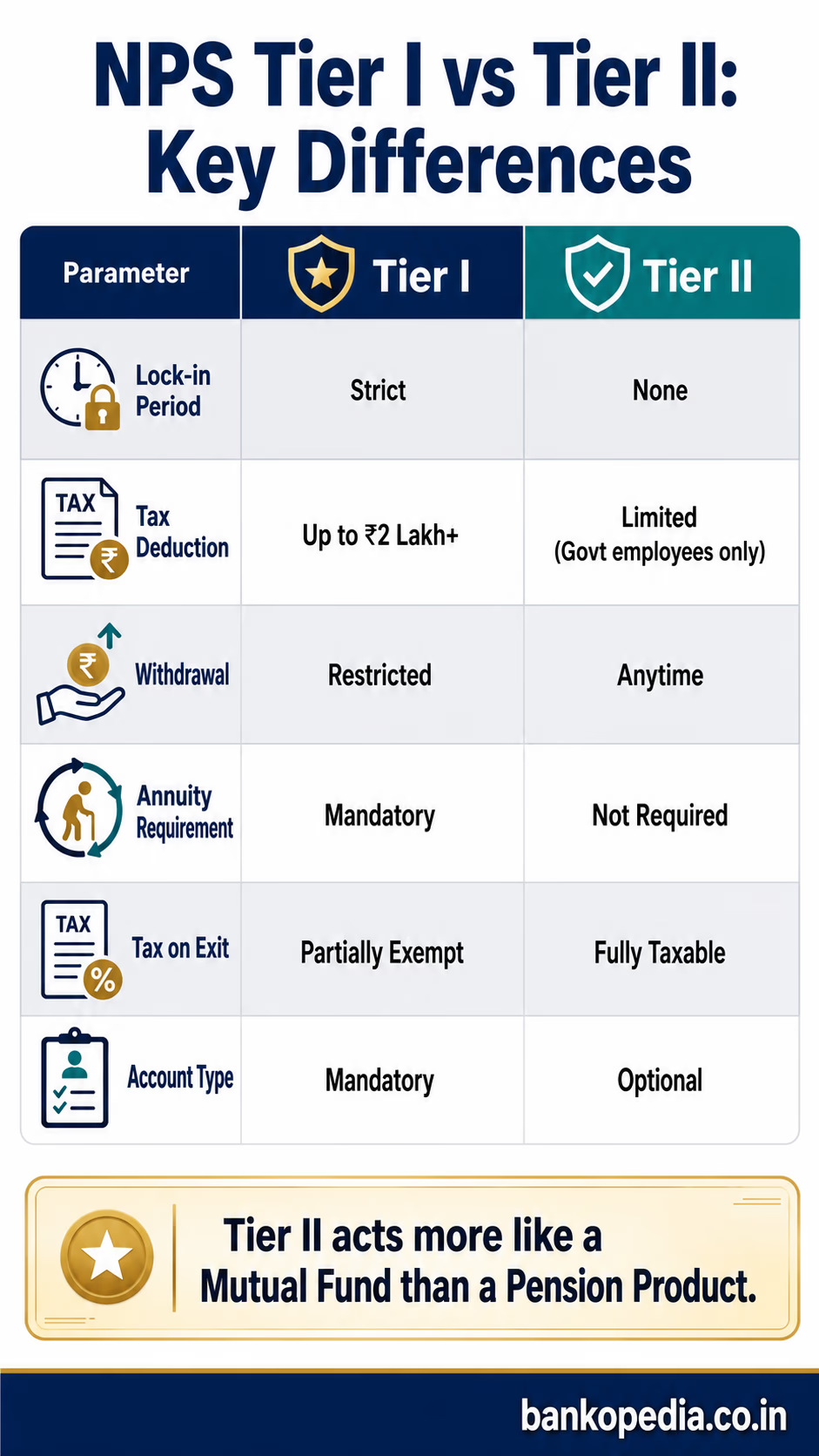

Tier I is the primary, mandatory pension account. It comes with strict withdrawal restrictions — partial withdrawals are permitted only under specific conditions (such as higher education, medical emergencies, or purchase of a house), and the bulk of the corpus must be used to purchase an annuity upon retirement. In return for this lock-in, Tier I offers substantial tax advantages:

Deduction of up to ₹1.5 lakh under Section 80C of the Income Tax Act

An additional deduction of up to ₹50,000 under Section 80CCD(1B)

Employer contributions deductible under Section 80CCD(2), up to 10% of basic salary for private employees and 14% for central government employees

Partial tax-free withdrawals and tax-free lump sum at maturity (up to 60% of the corpus)

NPS Tier II: The Voluntary, Flexible Investment Account

Tier II is an optional, add-on account that can only be opened if you already hold an active Tier I account. It functions more like a mutual fund than a pension product. Key features include:

No lock-in period: Funds can be withdrawn at any time without restriction

No mandatory annuity: The entire corpus can be withdrawn as a lump sum

Flexible investment choices: Subscribers can choose across asset classes — equity (Class E), corporate bonds (Class C), and government securities (Class G)

Limited tax benefits: Only central government employees investing in Tier II with a 3-year lock-in can claim deduction under Section 80C

This flexibility is a double-edged sword. While it makes Tier II attractive as a liquid savings vehicle, it also means the tax treatment is far less favourable compared to Tier I. And this is precisely where most investors get caught off guard.

How Are NPS Tier II Withdrawals Taxed: LTCG, STCG, or Income Tax Slab?

This is the crux of the matter, and the answer is nuanced. The NPS Tier II withdrawal tax rules do not follow a single uniform framework — they depend on the holding period, the asset class chosen, and the subscriber's residential status and income bracket.

The Overarching Principle: No Special Tax Status

Unlike Tier I, where significant portions of the corpus enjoy tax-exempt status, NPS Tier II withdrawals are fully taxable. There is no Section 10(12A) exemption available for Tier II accounts. The gains are treated much like those from market-linked investments, but with an important caveat: they are not treated as capital gains across the board.

PFRDA and Income Tax Act Position

As per the current Income Tax Act provisions and the guidance issued through PFRDA circulars, withdrawals from NPS Tier II accounts are treated as follows:

The gains from NPS Tier II withdrawals are taxable as income from other sources or as capital gains, depending on the nature of the underlying fund and the applicable judicial interpretation — but the predominant and safer tax position treats them as income taxable at the applicable slab rate.

Why the LTCG/STCG Question Is Complicated

Many investors assume that since NPS Tier II invests in equity funds, the long-term capital gains (LTCG) tax rate of 12.5% (post the Finance Act 2024 revision, which raised it from 10%) or the short-term capital gains (STCG) rate of 20% (revised from 15%) should apply. This reasoning is understandable but legally imprecise for the following reasons:

NPS Tier II units are not classified as "equity-oriented mutual fund" units under Section 112A or Section 111A of the Income Tax Act. Those provisions apply specifically to listed equity shares or units of equity-oriented funds as defined under the Act.

The NPS Tier II account, even when invested in Class E (equity), is a pension fund structure managed by PFRDA-registered Pension Fund Managers (PFMs), not a SEBI-registered mutual fund scheme. SEBI regulates mutual funds under the SEBI (Mutual Funds) Regulations, 1996, while PFRDA governs NPS under the PFRDA Act, 2013.

Because NPS units don't qualify as capital assets in the conventional sense used by the Income Tax Act for listed securities, the concessional capital gains tax rates do not straightforwardly apply.

The Slab Rate Default

In the absence of a specific provision granting capital gains treatment, the income tax department's position — and the position most tax practitioners advise their clients to adopt — is that NPS Tier II withdrawals are taxed at the individual's applicable income tax slab rate. This means:

For investors in the 30% tax bracket, gains from Tier II withdrawals will attract a 30% tax (plus applicable surcharge and cess)

There is no benefit of indexation

There is no threshold exemption specific to NPS Tier II gains

The gains are added to total income and taxed accordingly

This is a significantly less favourable outcome than investing in an equity mutual fund (which would attract 12.5% LTCG after ₹1.25 lakh exemption) or even a debt mutual fund (which, post April 2023, is also taxed at slab rate — but with the expectation of future regulatory clarity).

Tax Treatment by Asset Class: Equity, Corporate Bonds, and Government Securities

NPS Tier II allows investors to allocate across three primary asset classes. Let us examine how the tax treatment plays out for each, and why the asset class chosen does not materially change the tax outcome at the subscriber level — even though the underlying assets themselves are subject to different tax rules at the fund level.

Class E (Equity): Active and Auto Choice

Class E invests predominantly in equity and equity-related instruments. The Pension Fund Manager (PFM) managing the Class E portfolio pays taxes at the fund level as applicable to institutional equity investors. However, when a subscriber withdraws from their Tier II account — receiving their units redeemed at NAV — the gains to the subscriber are still treated as ordinary income, not as LTCG from equity.

This is a critical distinction. The fund benefits from equity tax treatment internally; the subscriber does not receive a pass-through of those benefits in the form of concessional tax rates. Think of it as analogous to receiving a dividend from a company — the company has already paid corporate tax, but the dividend received is still taxable in the hands of the recipient at slab rates.

Class C (Corporate Bonds)

Class C invests in investment-grade corporate bonds and other fixed income instruments. For traditional debt mutual funds, gains are taxed at slab rate post April 2023. NPS Tier II Class C investments follow a similar logic — gains on withdrawal are taxed at the subscriber's applicable slab rate. There is no indexation benefit available, making the post-tax returns potentially lower than what an investor might expect from a comparable fixed income product.

Class G (Government Securities)

Class G invests in central and state government securities, treasury bills, and sovereign instruments. Despite the underlying sovereign guarantee on the instruments themselves, the tax treatment for the NPS Tier II subscriber remains unchanged — withdrawals are taxed at slab rate. There is no special treatment for government securities held through the NPS Tier II route, unlike the treatment available to certain institutional investors or sovereign bond holders under specific RBI-designated frameworks.

Alternative Assets (Class A)

For subscribers who have access to Class A (alternative assets such as infrastructure investment trusts and real estate investment trusts), the tax position is similarly governed by the slab rate framework. Class A is generally accessible only to sophisticated investors and is subject to a cap on allocation.

A Summary Table for Quick Reference

Class E (Equity): Gains on Tier II withdrawal taxed at income tax slab rate

Class C (Corporate Bonds): Gains on Tier II withdrawal taxed at income tax slab rate

Class G (Government Securities): Gains on Tier II withdrawal taxed at income tax slab rate

Class A (Alternative Assets): Gains on Tier II withdrawal taxed at income tax slab rate

The consistent conclusion: asset class selection does not change the tax rate for the subscriber, though it does affect the pre-tax return profile and risk characteristics of the portfolio.

Key Mistakes to Avoid When Withdrawing from NPS Tier II

Given the complexity and the relative lack of awareness around NPS Tier II withdrawal taxation, investors routinely make costly errors. Here are the most consequential mistakes — and how to avoid them.

Mistake 1: Assuming LTCG Treatment for Equity Allocations

The most common error is assuming that holding NPS Tier II Class E units for more than one year automatically qualifies the gains for the 12.5% LTCG rate applicable to equity-oriented funds. As established above, this assumption is incorrect. Filing your income tax return with LTCG treatment for NPS Tier II gains could attract scrutiny from the Income Tax Department and result in demand notices, penalties, and interest under Sections 234B and 234C.

Mistake 2: Not Accounting for the Tax Liability Before Withdrawing

Because NPS Tier II withdrawals are not subject to Tax Deducted at Source (TDS) in most cases (unlike fixed deposits, for instance), subscribers may receive the full withdrawal amount and mistakenly believe it is tax-free. The tax liability must be self-assessed and disclosed in the annual Income Tax Return. Failure to do so constitutes tax evasion, even if unintentional.

Mistake 3: Overlapping Withdrawals with High-Income Years

Since gains are taxed at the slab rate, withdrawing a large NPS Tier II corpus in a year when your other income is already high (salary, business income, capital gains from other investments) will push you into the 30% bracket — or deepen your exposure to surcharge. Strategic withdrawal planning — for example, withdrawing in a year of lower income such as the first year of retirement — can significantly reduce the overall tax burden.

Mistake 4: Ignoring the Exception for Central Government Employees

Central government employees who invest in NPS Tier II with a mandatory 3-year lock-in (notified under the NPS Tier II Tax Saver Scheme) can claim Section 80C deductions. However, the withdrawal from this specific scheme after the lock-in period is taxed differently. Many government employees confuse this scheme with a regular Tier II account. The tax treatment on withdrawal for the notified scheme aligns with Tier I partial withdrawal rules and requires careful documentation.

Mistake 5: Failing to Report Gains Under the Correct Head of Income

When filing ITR, taxpayers must classify income correctly. NPS Tier II withdrawal gains should typically be reported under "Income from Other Sources" in the absence of a clear capital gains classification. Reporting them under "Capital Gains" without proper legal backing or a qualified tax opinion could attract misclassification penalties.

Mistake 6: Comparing NPS Tier II Directly with Mutual Funds Without Tax Adjustment

Financial advisors and investors frequently compare NPS Tier II returns with mutual fund returns on a gross basis. This comparison is misleading. An equity mutual fund held for over a year attracts 12.5% LTCG (with the first ₹1.25 lakh exempt), while NPS Tier II gains are taxed at up to 30% at the slab rate. For a high-income investor, the post-tax return differential can be substantial — sometimes making a regular equity mutual fund significantly superior to NPS Tier II for non-pension savings goals.

Practical Conclusion: Use NPS Tier II Strategically, Not Indiscriminately

The NPS Tier II account is a powerful and flexible instrument when used appropriately. Its absence of lock-in makes it attractive for medium-term financial goals, and the low expense ratios of PFRDA-registered PFMs make it cost-competitive with mutual funds. However, the tax inefficiency on withdrawal — a direct consequence of the NPS Tier II withdrawal tax rules — means it is not the optimal vehicle for every investor or every financial goal.

Here is a practical framework for decision-making:

For long-term retirement savings: Maximise Tier I contributions first, extracting full tax benefits under Sections 80CCD(1), 80CCD(1B), and 80CCD(2) before deploying capital in Tier II.

For medium-term goals (3–7 years): Compare NPS Tier II post-tax returns carefully against ELSS funds, PPF, and balanced advantage funds, accounting for your marginal tax rate.

For central government employees: The NPS Tier II Tax Saver Scheme with its 3-year lock-in remains a compelling option if you have exhausted the ₹1.5 lakh Section 80C limit through other instruments.

For high-income individuals (30% bracket): The tax drag on Tier II withdrawals is significant. Consult a qualified chartered accountant or tax advisor before making large withdrawals, and explore staggered withdrawal strategies.

As PFRDA continues to expand the NPS ecosystem and discussions around improving the tax parity of Tier II with mutual funds gain legislative attention, the rules may evolve. Staying updated through authoritative sources — and avoiding the trap of misapplying mutual fund tax logic to NPS Tier II — will ensure that your retirement and savings strategy remains both legally compliant and financially sound.

For more in-depth guides on NPS, taxation of financial instruments, and retirement planning in India, explore the Bankopedia knowledge base at bankopedia.co.in.