EPF Wage Ceiling in India: Understanding the Limit, Its History, and What a Revision Would Mean

The EPF wage ceiling limit in India sits at the centre of one of the country's most consequential retirement security debates. Currently fixed at ₹15,000 per month — a threshold that has remained unchanged since September 2014 — the statutory wage cap for Employees' Provident Fund coverage determines who is mandatorily enrolled in the social security net and who falls outside it. With the government reportedly revisiting a proposal to raise this ceiling, millions of workers, thousands of employers, and the Employees' Provident Fund Organisation (EPFO) itself stand at an inflection point. For banking and finance professionals tracking India's evolving social security architecture, understanding what this ceiling is, how it has evolved, and what its revision would imply is not merely academic — it is essential groundwork for advising clients, assessing institutional risk, and understanding household financial behaviour.

What Is the EPF Wage Ceiling and How Does It Work

The Employees' Provident Fund and Miscellaneous Provisions Act, 1952, mandates that every establishment employing 20 or more workers must enrol eligible employees in the EPF scheme. The operative word here is eligible — and eligibility is defined, in significant part, by the wage ceiling.

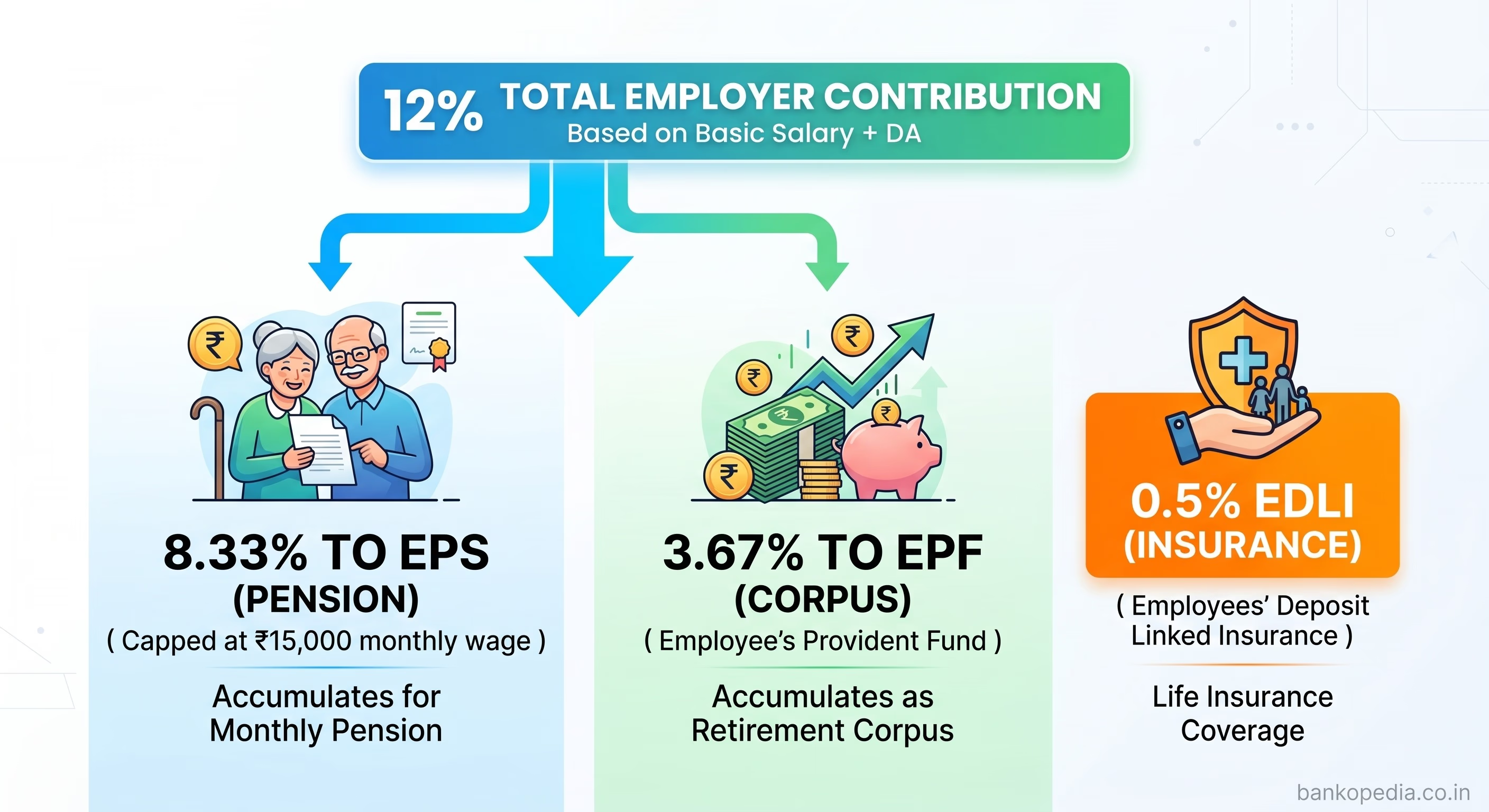

Under the current framework, any employee earning a basic salary plus dearness allowance (DA) of up to ₹15,000 per month is compulsorily covered under the EPF scheme. Both the employer and the employee contribute 12% of this basic wage to the provident fund. The employee's entire 12% goes into the EPF account, while the employer's 12% is split: 8.33% flows into the Employees' Pension Scheme (EPS) and the remaining 3.67% goes into the EPF corpus. Additionally, the employer contributes 0.5% towards the Employees' Deposit Linked Insurance (EDLI) scheme.

It is important to distinguish between two categories of workers in this context:

Mandatorily covered employees: Those earning up to ₹15,000 per month in basic wages, for whom EPF membership is compulsory.

Voluntarily covered employees: Those earning above ₹15,000 per month who may choose to remain in or opt into the EPF system. These employees are classified as excluded employees for statutory purposes but can continue contributing if already members or if they voluntarily enrol.

The wage ceiling, therefore, does not cap how much a person can contribute — a higher-earning employee can contribute on their actual salary — but it determines the floor of mandatory inclusion. When the ceiling is low relative to prevailing wages, a large share of the workforce that earns above the threshold but is not already enrolled simply falls outside compulsory social security protection.

For EPS specifically, the ceiling matters even more sharply. The pensionable salary for EPS purposes is capped at ₹15,000 per month, which means the maximum monthly pension for a retiree after 35 years of service works out to approximately ₹7,500 — a figure that many labour economists consider inadequate given current living costs in Indian cities.

History of EPF Wage Ceiling Revisions in India

The EPF wage ceiling has been revised only a handful of times since the scheme's inception, and each revision has been a significant policy event with lasting implications for coverage breadth and EPFO's financial flows.

The Early Decades: ₹500 to ₹1,600

When the EPF scheme was launched in the early 1950s, the wage ceiling was a nominal figure consistent with the wage levels of that era. Through the 1960s and 1970s, the ceiling was revised periodically but remained modest. By the 1985, as industrialisation and organised-sector employment grew, the ceiling had moved to ₹1,600 per month — still covering a relatively narrow band of formal workers.

The 1990s Liberalisation Era: ₹3,500 to ₹5,000

Economic liberalisation in 1991 brought structural changes to the labour market. As wages in the formal sector rose and new industries emerged, the ceiling was revised upward. In 1990, the ceiling was raised to ₹3,500, and in 1994 it was further enhanced to ₹5,000 per month. These revisions were significant because they brought a larger share of the expanding organised workforce under mandatory social security protection at a time when India's services sector was beginning its steep growth trajectory.

2001: Ceiling Raised to ₹6,500

At the turn of the millennium, the ceiling was revised again to ₹6,500 per month. This remained in force for over a decade — an unusually long period of stagnation relative to the pace of wage growth witnessed during India's high-growth phase of the 2000s. As a result, by the late 2000s, the real value of the wage ceiling had eroded substantially, and a growing proportion of organised-sector workers technically fell outside mandatory EPF coverage simply because their salaries had outpaced the unchanged threshold.

2014: The Last Revision — ₹15,000

The most recent — and currently operative — revision came in September 2014, when the ceiling was raised from ₹6,500 to ₹15,000 per month. This was a significant jump of approximately 130% and represented a belated but substantial course correction. The 2014 revision brought millions of additional workers into the mandatory EPF net, expanded EPFO's subscriber base meaningfully, and increased contribution flows into the system. However, in the decade since, India's wage levels have continued to rise. The average basic salary across many entry-level corporate and manufacturing roles in urban centres now exceeds ₹15,000, meaning the ceiling has, once again, become progressively less reflective of the actual wage landscape.

"Each time the EPF wage ceiling has been revised, it has triggered a short-term surge in EPFO enrolments and a recalibration of employer payroll costs. The decade-long freeze since 2014 has allowed structural distortions to accumulate in ways that a fresh revision would need to address carefully."

The Current Proposal: A Revision to ₹21,000 or Higher?

Reports indicate that the government is revisiting a proposal to raise the EPF wage ceiling, with figures ranging from ₹21,000 to ₹25,000 per month under discussion. A revision at the higher end would represent an increase of roughly 67%, which, while substantial, would still fall short of fully compensating for the wage inflation witnessed since 2014. The proposal, if formalised, would require an amendment to the EPF and MP Act and notification through a gazette order, and would have wide-ranging implications for employees, employers, and EPFO's financial and administrative operations.

How a Higher Wage Cap Affects Employees, Employers, and EPFO

For Employees: Expanded Social Security, Lower Take-Home Pay

From an employee standpoint, a higher wage ceiling is a double-edged policy instrument. On one hand, it would extend mandatory retirement savings coverage to a broader swathe of the workforce — particularly those in the ₹15,001 to ₹25,000 monthly basic salary bracket who are currently excluded from compulsory enrolment. For this segment, which includes a significant portion of workers in manufacturing, logistics, retail, and entry-level services, mandatory enrolment means access to a tax-advantaged, government-backed savings vehicle, life insurance through EDLI, and — crucially — eligibility for the pension benefit under EPS.

On the other hand, mandatory EPF contribution directly reduces take-home pay. For a worker earning ₹20,000 in basic wages, a 12% employee contribution would amount to ₹2,400 per month withheld from immediate consumption. For lower-middle-income households with thin financial buffers, this can create short-term cash flow stress. Policymakers must weigh the long-term retirement security benefit against the immediate liquidity cost, particularly in a country where a large share of households remain financially constrained.

For Employers: Higher Compliance Costs and Payroll Restructuring

Employers — particularly small and medium enterprises (SMEs) that constitute the backbone of India's organised employment — face a meaningful increase in their wage bill when the ceiling is raised. If the ceiling moves to ₹21,000, employers would be required to contribute 12% of the higher base for all newly covered employees, in addition to their existing EPF-covered workforce. This incremental cost, when aggregated across hundreds or thousands of employees, can run into crores of rupees annually for mid-sized firms.

There is also a well-documented tendency among some employers to restructure compensation architecture in response to EPF ceiling changes — splitting salary into components that do not attract PF deductions (house rent allowance, special allowance, etc.) to keep the EPF-applicable basic wage below the ceiling. While this practice is legally contested and has been the subject of Supreme Court scrutiny, it remains prevalent. A higher ceiling could accelerate such restructuring unless accompanied by stronger enforcement mechanisms.

However, it should also be noted that from a talent attraction perspective, EPF enrolment is valued by many employees as a benefit, and formalisation of previously excluded workers can improve employer credibility and regulatory compliance standing.

For EPFO: Asset Growth, Operational Scale, and Investment Implications

For EPFO — which manages a corpus of over ₹22 lakh crore and serves more than 7 crore active subscribers as of recent data — a wage ceiling revision would have significant financial and operational consequences. A larger mandatory membership base means higher contribution inflows, greater assets under management, and expanded capacity to generate investment returns. EPFO invests its corpus across government securities, bonds, and — since 2015 — equity exchange-traded funds (ETFs), in proportions regulated by the Finance Ministry's investment guidelines.

The increase in investible corpus would amplify EPFO's already considerable footprint in India's debt and equity markets. Given that EPFO is a major buyer of central and state government securities, its expanded scale would have macroeconomic implications for bond market liquidity and pricing — a consideration that would not be lost on the Reserve Bank of India (RBI) as it manages monetary conditions and the government securities market.

Operationally, EPFO would need to onboard a large number of new employers and employees into its Universal Account Number (UAN) ecosystem, upgrade its claims processing infrastructure, and manage the EPS pension liability implications of a broader contributor base. The pension arithmetic is particularly sensitive: bringing more workers into EPS at higher salary levels increases the long-term pension payout obligation, which must be funded through contributions and government support.

Financial Inclusion Implications of Expanding PF Coverage

The EPF wage ceiling debate is, at its core, a financial inclusion debate. India's formal social security infrastructure — despite decades of effort — still leaves large segments of the workforce without structured retirement savings or life cover. Raising the wage ceiling is one lever among several to close this gap, but its efficacy must be assessed in context.

Formalisation of the Workforce

India's formal employment landscape has expanded significantly in the post-pandemic period, partly aided by EPFO's own enrolment data showing net new additions in the range of 15–18 lakh subscribers per month in recent years. A higher wage ceiling would bring more of the so-called "near-formal" workforce — workers who are employed by registered establishments but whose salaries just exceed the current ₹15,000 threshold — into the mandatory net. This has cascading benefits: it creates a digital financial identity through the UAN, enables access to EPFO's online withdrawal and advance facilities, and builds a savings habit from the early stages of a worker's career.

Linkages to Banking and Credit Ecosystems

From the perspective of India's banking sector, EPF membership has become an increasingly important marker of financial identity and creditworthiness. Banks and NBFCs use EPFO contribution history as a proxy for stable employment and income verification — particularly for personal loan, home loan, and credit card underwriting. Expanding EPF coverage thus deepens the pool of formally verifiable borrowers, potentially improving credit access for lower-middle-income workers who have historically been underserved by mainstream financial institutions.

NABARD and microfinance institutions operating in semi-urban areas have long highlighted the difficulty of assessing creditworthiness for workers without formal financial records. EPF membership, especially when linked to the Jan Dhan–Aadhaar–Mobile (JAM) trinity, can serve as an anchor for financial identity that unlocks a range of products across banking, insurance, and investment.

Gender and Sectoral Dimensions

A higher EPF ceiling would disproportionately benefit workers in sectors where female employment is concentrated at salary levels just above the current ₹15,000 threshold — including garments and textiles, healthcare support staff, and retail. Extending mandatory EPF coverage to these workers would help narrow the gender gap in retirement savings, an area of persistent concern for Indian social policy.

Challenges: Informal Sector and Compliance Gaps

It must be acknowledged that the EPF ceiling revision, however well-designed, addresses only a slice of the broader informal employment challenge. Over 90% of India's workforce remains in the informal sector, entirely outside the EPF net regardless of any ceiling revision. For this population, instruments such as the Pradhan Mantri Shram Yogi Maan-dhan (PM-SYM) pension scheme and NPS Lite (Swavalamban) are more relevant, though their uptake has been limited. The ceiling revision is thus best understood as a measure to deepen coverage within the already-formal segment, rather than a solution to the informal employment challenge.

Conclusion: A Long-Overdue Recalibration With Far-Reaching Consequences

The EPF wage ceiling limit in India is not merely a technical threshold — it is a policy parameter that shapes the retirement security architecture for tens of millions of workers, the compliance economics of hundreds of thousands of employers, and the investment strategy of one of the world's largest provident fund organisations. The decade-long freeze at ₹15,000 per month has allowed a growing mismatch between the ceiling and actual wage realities to undermine the inclusiveness of a scheme that was designed to be universal for the organised sector.

A revision — whether to ₹21,000 or a higher figure — would be a significant and overdue step. But its success will depend on accompanying measures: robust enforcement to prevent salary restructuring that circumvents the spirit of the revision, adequate EPFO administrative capacity to absorb the expanded membership, transparent management of the EPS pension liability, and coordinated outreach to newly covered workers to help them understand and utilise their entitlements.

For India's banking and finance community, the EPF ceiling revision is a development worth tracking closely. Its ripple effects — on household savings rates, debt market flows, corporate payroll costs, and credit underwriting benchmarks — will touch virtually every segment of the financial ecosystem. The social contract embedded in the EPF is simple: a small sacrifice from current income in exchange for security in old age. Ensuring that contract extends to the widest possible share of the workforce is both a social imperative and, ultimately, a macroeconomic necessity for a country navigating its demographic dividend with ambition and urgency.