Centre's Capex Loans to States: Fiscal Conditions, Allocation Mechanics, and Economic Impact

Among the more consequential yet underappreciated instruments in India's intergovernmental fiscal architecture, the Centre capex loan states India fiscal conditions framework has quietly reshaped how subnational governments finance long-gestation infrastructure projects. Formally structured under the Special Assistance to States for Capital Investment scheme — commonly referred to as the Scheme for Special Assistance to States — these interest-free or concessional loans from the Union government have grown from a pandemic-era stimulus measure into a durable pillar of cooperative federalism. Understanding how they work, why conditions are attached, and what consequences they carry for public finance, bond markets, and real economic growth is essential knowledge for any banking or finance professional tracking India's macroeconomic trajectory.

"States are the primary engines of capital expenditure in India, accounting for roughly 60 to 65 per cent of total public sector capex. Strengthening their financing capacity directly translates into faster infrastructure delivery."

What Are Interest-Free Capex Loans Given by the Centre to States?

The Special Assistance to States for Capital Investment scheme was first introduced in the Union Budget for FY 2020-21 as a ₹12,000 crore allocation to nudge states toward higher capital spending at a time when private investment had stalled and pandemic-related disruptions had compressed fiscal headroom. Since then, the scheme has expanded substantially. By FY 2023-24, the total outlay under the scheme had risen to ₹1.3 lakh crore, a figure that underscores its transformation from an emergency measure to a structural financing instrument.

The core feature of these loans is their concessional or interest-free nature. Unlike market borrowings through State Development Loans (SDLs) — which states raise through auctions managed by the Reserve Bank of India and which currently carry yields in the range of 7 to 7.5 per cent — these Centre-provided loans carry zero interest for a tenure of fifty years. In practical terms, the long moratorium and absence of interest make them quasi-grants with a nominal repayment obligation, effectively reducing the cost of capital for state governments to near zero.

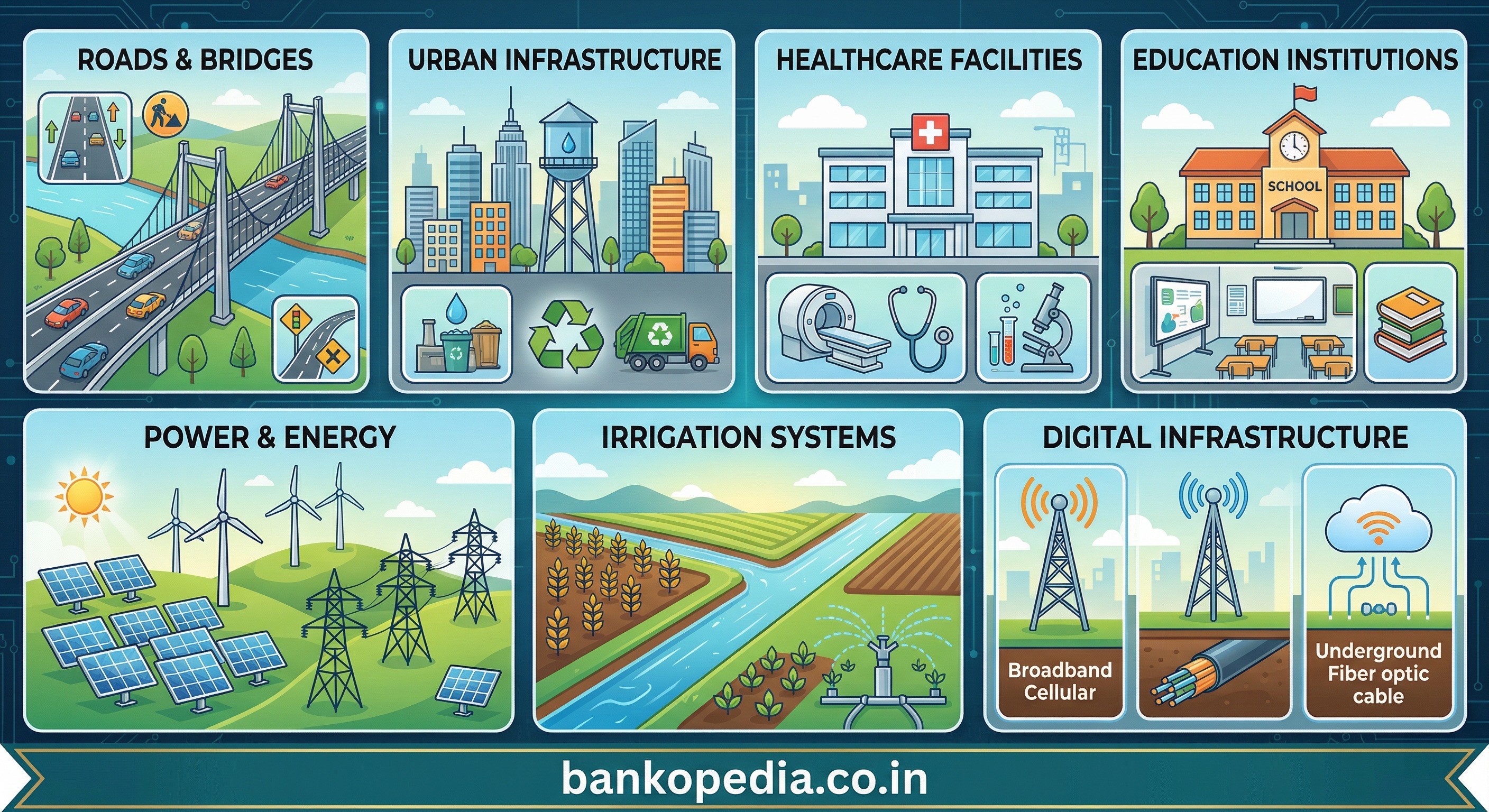

Eligible Uses: Where Can States Deploy These Funds?

The scheme is explicitly designed to crowd in productive, long-term capital formation rather than supplement revenue expenditure. Eligible uses typically include:

Road and bridge construction at the state and district level, including rural connectivity projects that complement national highway programmes

Urban infrastructure such as water supply, sewerage, and solid waste management systems in cities and towns

Health and education infrastructure, including hospital buildings, medical colleges, school construction, and laboratory upgrades

Power sector investments, particularly distribution network upgrades and renewable energy integration

Irrigation and flood management projects, including canal renovation and reservoir capacity expansion

Digital and optical fibre connectivity at the last-mile level, complementing national broadband initiatives

Police infrastructure and judicial infrastructure in some tranches

A critical safeguard built into the scheme is the additionality principle. States must demonstrate that the borrowed funds are genuinely additional to their existing capital expenditure plans. The Department of Expenditure under the Ministry of Finance monitors this through quarterly utilisation certificates and project-specific documentation, preventing states from simply substituting cheaper Centre loans for planned market borrowings without increasing their actual capital outlay.

How Does This Differ from Other Central Transfers?

It is important to distinguish these loans from other forms of central assistance to states. Tax devolution under the Finance Commission's formula is an unconditional transfer based on a state's share of the divisible pool. Centrally Sponsored Schemes (CSS) involve co-financing arrangements with conditionalities tied to specific programme outputs. Capex loans, by contrast, are purpose-bound but relatively flexible within a broad infrastructure rubric, and — crucially — they are loans that must eventually be repaid, preserving some fiscal discipline incentive on the part of states.

Why Does the Centre Attach Fiscal Discipline Conditions to These Loans?

The integration of fiscal discipline conditions into the capex loan framework is not accidental. It reflects a deliberate design choice rooted in the moral hazard problem inherent in any concessional lending arrangement. If states receive cheap financing with no strings attached, the incentive to rationalise revenue expenditure, control subsidies, or improve own-tax revenue mobilisation is significantly weakened.

Recent news reports have confirmed that a meaningful portion of the state capex loan allocation is explicitly tied to fiscal discipline benchmarks. This conditionality architecture typically operates in tranches, with a base tranche released on demonstration of eligible project expenditure, and additional tranches contingent on states meeting specific reform milestones.

Key Reform Conditions Linked to Loan Disbursement

Over the years, the Union government has bundled a wide range of reform conditionalities with the capex loan scheme. These have included:

Own Tax Revenue (OTR) improvement targets: States must show measurable improvement in collecting GST, stamp duty, excise, and other own-source revenues relative to their GSDP, demonstrating that Centre assistance does not substitute for state fiscal effort.

Reduction in non-merit subsidies: Some tranches require states to rationalise power subsidies through direct benefit transfer (DBT) mechanisms or implement electricity tariff revisions, aligning with UDAY-like reform frameworks.

Disinvestment and monetisation of state PSUs: States are encouraged to list or monetise public sector undertaking assets, freeing up balance sheet capacity and improving resource allocation efficiency.

Urban local body (ULB) finance reforms: Strengthening property tax collection, improving ULB creditworthiness, and enabling municipal bond markets are among the conditionalities linked to urban infrastructure tranches. SEBI has been working alongside the Centre to encourage states to develop their municipal bond frameworks, a process that complements the capex loan architecture.

Land record digitisation and single-window clearances: These ease-of-doing-business reforms are designed to improve the investment climate at the state level, making public capex more effective at crowding in private investment.

FRBM compliance: States must remain within their Fiscal Responsibility and Budget Management Act limits on fiscal deficit — typically 3 per cent of GSDP, with an additional 0.5 per cent allowed for power sector reforms — to remain eligible for disbursements.

The fiscal conditionality model draws partly from the experience of international development finance institutions. The World Bank and Asian Development Bank routinely embed policy reform triggers in programme loans to sovereign borrowers. The Centre has adapted this discipline to the Indian federal context, where the Finance Commission and RBI jointly shape the borrowing space available to states.

The Debate Around Conditionality

Not all states — particularly larger, poorer ones with constrained administrative capacity — view these conditionalities favourably. Critics argue that attaching reform benchmarks to emergency or stimulus-category lending places disproportionate burdens on states already grappling with legacy fiscal stress. Proponents counter that without such conditions, the scheme risks becoming a fiscal transfer mechanism that entrenches inefficiency rather than catalysing structural improvement. The balance between cooperative federalism and disciplined resource allocation remains a live debate in Indian public finance circles.

How Are Capex Loan Allocations Decided and Disbursed Each Year?

The annual allocation process for state capex loans involves multiple institutional actors and follows a structured sequence that begins well before the Union Budget is presented on February 1 each year.

Allocation Methodology

The total scheme outlay is determined by the Union Finance Ministry in consultation with the NITI Aayog and the relevant sectoral ministries. Within the total envelope, allocations to individual states are typically based on a combination of factors:

Population share, which ensures larger states receive proportionately larger allocations

Per capita income or GSDP, with an inverse weighting that directs more resources to economically weaker states

Past utilisation performance, rewarding states that have demonstrated capacity to absorb and deploy capital funds efficiently

Reform compliance track record, assessed on the basis of reform milestones from the prior financial year

A portion of the annual allocation — sometimes described as a performance or incentive tranche — is kept aside and distributed based on competitive rankings across reform parameters. This creates an element of fiscal federalism that incentivises states to outperform peers on measurable governance outcomes.

Disbursement Mechanics and the Role of the Department of Expenditure

Disbursements are managed by the Department of Expenditure within the Ministry of Finance and typically occur in quarterly or bi-annual tranches following the submission of:

Utilisation certificates for prior disbursements, certified by the respective state finance departments and countersigned by auditors

Project-level expenditure statements identifying specific works undertaken

Compliance certificates for reform conditionalities applicable to that tranche

The RBI plays an indirect but important role in this architecture. Since state borrowings — whether market-based SDLs or Centre loans — affect the overall consolidated public sector borrowing requirement, the RBI monitors aggregate state fiscal positions through its annual State Finances: A Study of Budgets publication. This surveillance function helps the central bank calibrate its assessment of system-wide liquidity and sovereign risk.

The Intersection with NABARD and Other Institutional Channels

For certain sectoral components — particularly rural infrastructure and irrigation — NABARD acts as a channel partner. Under the Rural Infrastructure Development Fund (RIDF), NABARD provides financing to states at concessional rates, functioning as a complement rather than a substitute for the direct capex loan scheme. States with strong agricultural and rural infrastructure pipelines often draw from both windows simultaneously, stacking concessional finance to maximise capital investment leverage.

Impact of State Capex Financing on Infrastructure Growth and Bond Markets

The macroeconomic and market consequences of the Centre's capex loan programme extend well beyond government balance sheets. Over the four years that the scheme has operated at scale, observable impacts have emerged across infrastructure delivery, private investment patterns, and the State Development Loan market.

Infrastructure Delivery: Measurable Gains

India's public capital expenditure as a share of GDP has risen meaningfully since FY 2020-21, driven in roughly equal measure by the Centre's own capex push and the state-level amplification enabled by these loans. National highway construction has been a visible output, but less-discussed gains in irrigation coverage, rural roads under PMGSY, and state urban transport investments are also traceable to enhanced state capex financing capacity.

The multiplier effect of public capital expenditure on GDP — estimated by various studies to range between 2.5 and 3.5 in the Indian context over a medium-term horizon — means that each rupee of state capex produces a disproportionate return in output and employment. For banking professionals, this translates into improved credit demand in construction, manufacturing, and services sectors in states that actively deploy these funds.

Private Investment Crowding-In

A central hypothesis behind the capex loan programme is that public infrastructure investment crowds in private capital by reducing logistics costs, improving connectivity, and creating productive assets. Early empirical evidence is encouraging. States that have shown high capex loan utilisation rates have, in several cases, also attracted higher industrial project announcements in subsequent years. While causality is difficult to establish cleanly, the directional relationship is consistent with the theoretical framework.

Effects on the State Development Loan Market

This is where the programme becomes directly relevant to fixed income market participants and banking institutions that hold SDLs on their balance sheets. By substituting expensive market borrowing with zero-cost Centre loans, states that effectively utilise the capex scheme reduce their net market borrowing requirements. This has two important consequences:

SDL supply reduction: Lower gross issuance of SDLs at the margin eases supply pressure on the bond market. Given that public sector banks, insurance companies, and provident funds are the dominant buyers of SDLs, any reduction in supply — holding demand constant — supports SDL prices and compresses yield spreads over G-Secs.

State fiscal position improvement: Reduced interest burden from market borrowings improves the interest-to-revenue-receipts ratio for states, a metric closely watched by credit analysts and rating agencies. Improved ratios, in turn, may support lower SDL yield premiums over time.

SEBI has also been exploring frameworks, in coordination with market participants and the RBI, to improve the depth and transparency of the SDL market. Efforts to standardise SDL documentation and encourage wider institutional participation complement the capex loan programme by potentially making state market borrowings — when required — more efficient and less costly.

Risks and Limitations

The programme is not without risks. States with weak project preparation capacity may face absorption constraints, leaving allocated funds undrawn. Political cycles can distort spending toward visible projects rather than high-return investments. And the accumulation of fifty-year liabilities — even at zero interest — adds to the long-run sovereign obligation of states, requiring careful tracking within FRBM frameworks. The RBI's annual assessment of state finances provides a useful public monitoring function, but the quality of project-level auditing remains variable across states.

Conclusion: A Maturing Instrument in India's Fiscal Federalism Toolkit

The Centre's capex loan programme to states has evolved from a countercyclical fiscal stimulus into a sophisticated instrument of cooperative federalism — one that blends concessional financing with structural reform incentives in ways that few other intergovernmental transfer mechanisms attempt. For Indian banking and finance professionals, its implications span public sector balance sheet dynamics, SDL market behaviour, credit demand across infrastructure-linked sectors, and the broader macroeconomic environment in which institutions like the RBI calibrate monetary policy and financial stability assessments.

As India accelerates its infrastructure investment agenda toward the ₹111 lakh crore National Infrastructure Pipeline and beyond, the role of state governments as primary capex executors will only grow. The Centre's capex loan framework — provided it maintains its conditionality integrity and improves absorption-side efficiency — offers a credible and fiscally responsible mechanism to finance that ambition without crowding out private investment or compromising monetary policy transmission.

For analysts, investors, and banking professionals monitoring India's public finance landscape, tracking the annual scheme allocation, state-level utilisation rates, and reform compliance records provides a leading indicator of both infrastructure pipeline momentum and the fiscal health trajectories of individual states — intelligence that is increasingly indispensable in a market where subnational credit dynamics shape everything from SDL spreads to sectoral credit growth.