Loan Against Silver in India: A Practical Guide for Borrowers

When most Indians think of pledging precious metals for a quick loan, gold naturally dominates the conversation. Yet loan against silver in India is a quietly growing credit product that deserves far more attention than it receives. Silver, long regarded as the "poor man's gold," has historically served as a store of value in Indian households — from ornate silverware passed down generations to silver coins accumulated during festivals. As silver prices have firmed up considerably over the past few years, pledging silver jewellery or artefacts can unlock meaningful liquidity without requiring you to liquidate an asset permanently. This article unpacks how the product works, how much you can realistically borrow, what interest rates and charges to expect, and how it compares with the more familiar gold loan — giving you a complete picture before you walk into a lender's branch.

What Is a Loan Against Silver and How Does It Work?

A loan against silver is a secured credit facility where the borrower pledges silver items — jewellery, coins, bars, or artefacts — as collateral with a lender in exchange for a loan disbursed against a percentage of the silver's assessed market value. The borrower retains ownership of the pledged silver throughout the loan tenure; the lender simply holds it as security. Once the loan is fully repaid, the silver is returned to the borrower in the same condition.

The mechanics broadly mirror those of a gold loan, which most Indians are already familiar with. Here is a step-by-step overview of how the process typically works:

Approach a lender: You visit the branch of a bank, non-banking financial company (NBFC), or cooperative society that offers silver loans. Not all lenders offer this product — it is considerably less standardised than gold loans.

Valuation of silver: A trained appraiser at the branch assesses the purity and weight of your silver. Unlike gold, where Bureau of Indian Standards (BIS) hallmarking is common, silver items often lack standardised hallmarks, which makes purity verification more involved. Lenders typically use acid testing or XRF (X-ray fluorescence) analysis.

Loan offer: Based on the assessed value of the silver and the lender's applicable Loan-to-Value (LTV) ratio, a loan amount is offered. You review the terms — interest rate, tenure, and charges.

Documentation: KYC documents (Aadhaar, PAN, address proof) are submitted. The process is minimal compared with unsecured loans.

Disbursement: Upon signing the pledge agreement, the loan amount is disbursed — often on the same day, directly to your bank account or in cash subject to applicable limits.

Repayment and retrieval: You repay principal and interest as per the agreed schedule. Once the dues are cleared, the pledged silver is returned. In case of default, the lender has the right to auction the silver to recover its dues.

It is worth noting that the Reserve Bank of India (RBI) regulates gold loans extensively — including specific LTV caps for banks and NBFCs — but silver loans do not enjoy the same degree of dedicated regulatory guidance. This makes it especially important for borrowers to scrutinise the terms offered by individual lenders rather than assuming uniform standards apply.

How Much Can You Borrow? Understanding LTV Ratios for Silver Loans

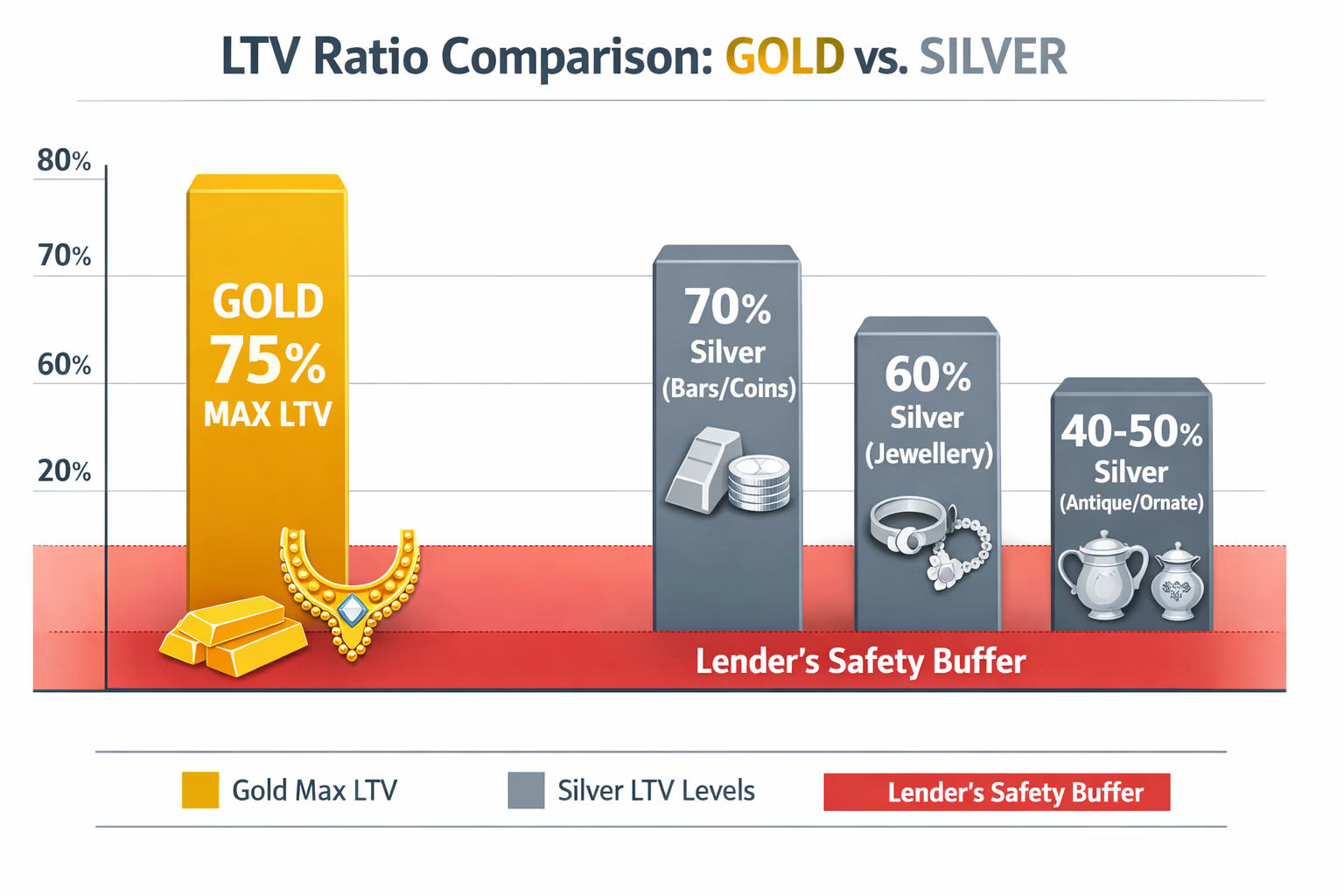

The Loan-to-Value (LTV) ratio is the single most critical number a silver loan borrower must understand. It determines what fraction of your silver's assessed market value the lender is willing to disburse as a loan. Unlike gold loans, where the RBI has explicitly capped the LTV at 75% for banks and most NBFCs, no equivalent blanket regulatory ceiling currently governs silver loans.

In practice, however, lenders tend to be notably more conservative with silver than with gold. The key reasons are:

Lower liquidity on default: In the event of a borrower default, auctioning silver is more complex than auctioning gold. The secondary market for silver ornaments and artefacts is thinner, meaning the lender faces greater risk of not recovering the full loan amount at auction.

Purity standardisation challenges: The absence of widespread hallmarking makes silver valuation less straightforward, introducing purity risk into the lender's calculations.

Given these factors, most lenders in India currently offer LTV ratios of 50% to 75% on silver loans, though the precise figure depends heavily on the lender category and the form of silver being pledged:

Silver bars and coins of known purity: These attract the highest LTV — sometimes up to 70–75% at select lenders — because purity verification is straightforward.

Silver jewellery: LTV is typically lower, often in the 50–65% range, because jewellery contains alloys and making charges that reduce the net silver content relative to gross weight.

Antique or ornate silverware: These attract the most conservative LTV, sometimes as low as 40–50%, given the difficulty in separating intrinsic metal value from craftsmanship value.

As a practical illustration: if you pledge silver bars assessed at ₹1,00,000 at current market prices, and the lender applies a 65% LTV, you would receive a loan of ₹65,000. The remaining ₹35,000 represents the lender's safety buffer against price fluctuations and recovery costs.

Borrowers should also be aware that lenders periodically revise LTV ratios in response to silver price movements. During periods of sharp silver price decline, lenders may issue margin calls — requesting additional collateral or partial repayment to restore the LTV to the permissible level. This is a risk that differentiates silver loans from fixed-rate secured products.

Interest Rates, Tenure, and Charges: What to Expect

Compared with unsecured personal loans, a loan against silver in India is relatively affordable — but it is not as competitively priced as gold loans, given the additional risks lenders perceive. Here is what borrowers should factor in:

Interest Rates

Interest rates on silver loans typically range from 10% to 18% per annum, depending on the lender type, the loan amount, and the tenure selected. For context:

Public sector banks: Tend to offer lower rates — approximately 10–13% per annum — but may be more selective about which silver items they accept as collateral.

Private sector banks: Rates generally fall between 12–16% per annum. Banks like HDFC Bank and ICICI Bank, both of which have reported robust credit growth in recent quarters, have been expanding their secured lending portfolios — though their silver loan offerings remain limited compared with their gold loan products.

Small finance banks: Institutions such as AU Small Finance Bank, which recently reported higher deposit growth relative to gross loan expansion, may offer competitive silver loan rates as they look to diversify their secured lending book. Expect rates in the 13–16% range.

NBFCs: Rates can vary widely — from 12% to 18% or higher — depending on the NBFC's cost of funds and risk appetite. Borrowers should be especially careful to read the fine print here.

Tenure

Silver loans are structurally short-term instruments. Most lenders offer tenures ranging from 3 months to 24 months, with 12 months being the most common. Some lenders allow rollovers or renewals upon reassessment of the silver's value, subject to prevailing LTV ratios at the time of renewal.

Processing and Other Charges

Beyond interest, borrowers should account for:

Processing fee: Typically 0.25% to 1% of the loan amount, sometimes subject to a minimum charge.

Valuation or assaying fee: A nominal charge for silver purity testing, usually ₹100–₹500 per visit.

Storage/insurance charges: Lenders charge for safekeeping the pledged silver. This is usually nominal but should be explicitly confirmed upfront.

Prepayment charges: Many lenders do not levy prepayment penalties on silver loans given their short tenures, but this must be confirmed in writing.

Auction notice and costs: In the event of default, borrowers may be liable for the administrative costs of the auction process as well.

Borrowers are advised to calculate the effective annual cost — aggregating interest, processing fees, and ancillary charges — rather than comparing interest rates in isolation.

Loan Against Silver vs Loan Against Gold: Key Differences

For most Indian borrowers, the choice is not simply whether to take a silver loan — it is whether silver or gold is the more suitable collateral given their holdings and borrowing needs. The two products differ across several important dimensions:

Regulatory Framework

Gold loans operate within a well-defined RBI regulatory architecture. The central bank has issued specific Master Directions for gold loans extended by banks and NBFCs, including the 75% LTV ceiling, guidelines on auction procedures, and restrictions on bullet repayment loans beyond a certain tenure. Silver loans currently lack comparable dedicated regulation, which creates both flexibility and risk — lender terms can vary significantly, and borrowers have fewer codified protections.

LTV Ratios

Gold loans typically allow an LTV of up to 75% (as mandated for regulated entities by the RBI). Silver loans, as discussed, offer 50–75% LTV at best — and often lower in practice — due to silver's higher price volatility and lower market liquidity.

Interest Rates

Gold loans generally attract lower interest rates than silver loans — often 7–12% per annum from banks and established NBFCs — reflecting the lower risk profile and the robust regulatory backing of the product. Silver loans command a moderate premium over these rates.

Lender Availability

Gold loans are offered by a vast ecosystem of lenders: public and private sector banks, specialised gold loan NBFCs (Muthoot Finance, Manappuram Finance), small finance banks, and cooperative banks. Silver loans are offered by a narrower range of lenders, predominantly certain public sector banks, some cooperative banks, and select regional NBFCs. The absence of specialised silver loan companies means the product is less competitive and less standardised.

Valuation Speed and Accuracy

Gold valuation is quick and reliable, aided by BIS hallmarking and standardised testing methods. Silver valuation takes longer and is less precise, which can delay disbursement and introduce subjectivity into the process.

Borrower Profile

Gold loans attract a broader demographic — urban and rural, individual and small business. Silver loans tend to be more relevant for households in states with strong silverware traditions (Rajasthan, Uttar Pradesh, Odisha) and for small artisans or traders who hold substantial silver inventory.

In summary: if you hold both gold and silver, gold is almost always the superior collateral — higher LTV, lower interest rate, and stronger regulatory protection. Silver loans are most appropriate when you have significant silver holdings and limited or no gold to pledge, or when diversifying collateral across multiple lenders.

Practical Considerations Before You Apply

A loan against silver in India can be a genuinely useful financial tool when used thoughtfully. Before proceeding, borrowers should keep the following in mind:

Compare lenders rigorously: Given the lack of standardised regulation, terms vary significantly. Request the complete schedule of charges — not just the headline interest rate — before signing any pledge agreement.

Understand the auction clause: Every silver loan agreement will specify conditions under which the lender can auction the pledged silver. Know these conditions precisely, and ensure you have a credible repayment plan before pledging heirloom or emotionally significant items.

Monitor silver prices: If silver prices fall sharply during your loan tenure, you may face a margin call. Having a contingency plan — whether additional collateral or partial prepayment — is prudent.

Check purity documentation: If you have receipts, assay certificates, or any purity documentation for your silver items, carry them to the lender. This can improve the LTV offered and speed up valuation.

Consider the tenure carefully: Silver loans are short-term instruments. Using them to fund long-gestation needs (home renovation, business capital expenditure) without a clear repayment timeline increases the risk of default and collateral loss.

As India's banking sector continues to mature — with institutions across the spectrum, from large private banks expanding credit portfolios to small finance banks deepening their secured lending reach — the silver loan segment is gradually receiving more institutional attention. For the informed borrower who understands the product's mechanics, limitations, and risks, it remains a legitimate and relatively accessible source of short-term secured credit. The key, as with all collateral-backed lending, is to borrow only what you can comfortably repay — and to treat your pledged silver not as permanently surrendered, but as temporarily working capital until you can reclaim it.