Bank vs NBFC Capital Adequacy Norms in India: A Comprehensive Guide

India's financial system rests on two broad pillars of regulated lending institutions: scheduled commercial banks and non-banking financial companies (NBFCs). While both mobilise funds and extend credit to the real economy, the regulatory architecture governing their capital buffers differs significantly. Understanding bank vs NBFC capital adequacy norms in India is not merely an academic exercise — it has direct consequences for credit availability, systemic risk, investor confidence, and the stability of India's broader financial sector. Recent moves by the Reserve Bank of India (RBI) to ease certain capital-related requirements for banks, including scrapping the Investment Fluctuation Reserve (IFR) mandate and relaxing Non-Performing Asset (NPA)-linked capital rules, have once again brought the capital adequacy conversation to the forefront. This article provides a structured, in-depth examination of how these norms are framed, how they differ between banks and NBFCs, and what the evolving regulatory direction signals for practitioners and stakeholders.

What Is Capital Adequacy and Why Does RBI Mandate It?

Capital adequacy, at its core, refers to the sufficiency of a financial institution's own funds relative to the risks embedded in its asset portfolio. It answers a fundamental question: if a bank or NBFC suffers significant losses on its loans and investments, does it have enough of its own resources to absorb those losses without defaulting on its obligations to depositors, creditors, and counterparties?

The RBI, as the primary regulator of both banks and most NBFCs, mandates minimum capital standards to achieve several interconnected objectives:

Depositor and creditor protection: Capital acts as a first line of defence. If losses erode assets, equity capital absorbs the blow before depositors or bondholders are affected.

Systemic stability: Under-capitalised institutions are more prone to runs and contagion. Adequate capital reduces the probability that the failure of one entity cascades across the financial system.

Discipline in risk-taking: Capital requirements create a cost for excessive risk. When institutions must maintain a proportion of their own funds against risky assets, they have a built-in incentive to price and manage risk prudently.

Regulatory confidence: Supervisors, rating agencies, and foreign investors use capital ratios as a signal of institutional health. Strong capital positions support India's credibility in global financial markets.

The conceptual foundation for modern capital adequacy draws from the Basel Accords — a series of international frameworks developed by the Basel Committee on Banking Supervision (BCBS) under the Bank for International Settlements (BIS). India has progressively adopted Basel I, Basel II, and Basel III norms for its scheduled commercial banks. NBFCs, however, operate under a separate, domestically crafted framework that reflects their different funding structures and systemic footprints.

"Capital is not just a regulatory requirement; it is the most honest signal a financial institution can send about its capacity to withstand stress."

Capital Adequacy Framework for Scheduled Commercial Banks in India

Basel III and the CRAR Requirement

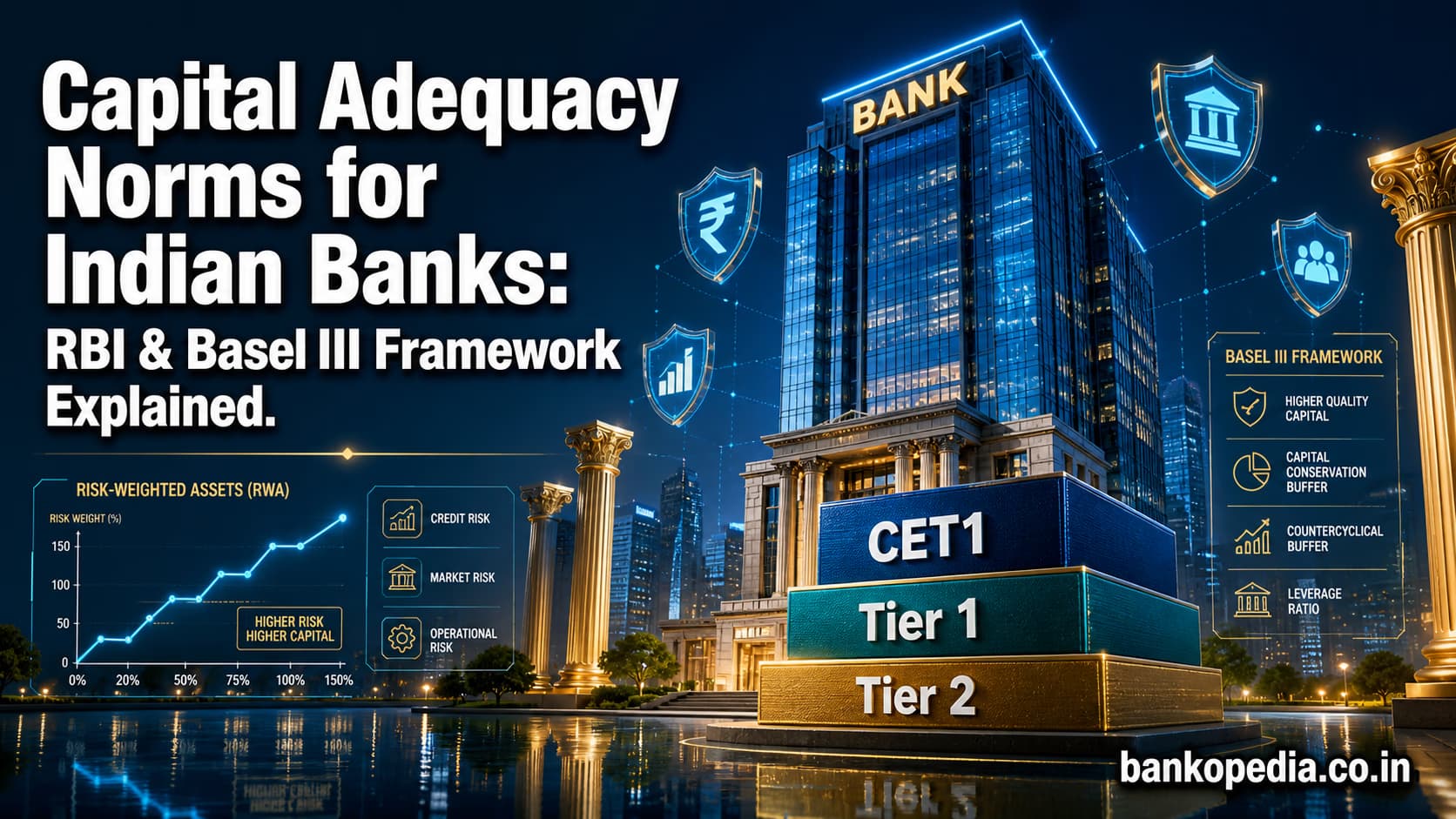

Scheduled commercial banks in India — including public sector banks, private sector banks, small finance banks, and foreign banks operating in India — are required to maintain a Capital to Risk-weighted Assets Ratio (CRAR) under the Basel III framework, as implemented by the RBI. The minimum CRAR mandated by the RBI stands at 9 percent, which is one percentage point higher than the 8 percent floor prescribed by the Basel Committee. This conservative calibration reflects the RBI's preference for a margin of safety given the structural vulnerabilities of the Indian credit ecosystem.

Components of Capital: Tier 1 and Tier 2

Under the Basel III framework adopted in India, a bank's regulatory capital is divided into two broad tiers:

Additional Tier 1 (AT1): Instruments like perpetual non-cumulative preference shares and eligible debt instruments with loss-absorption features. AT1 instruments can be written down or converted to equity under specified trigger conditions.

Tier 2 Capital (Gone-Concern Capital): Instruments and reserves designed to absorb losses in a winding-up scenario. This includes subordinated debt, general provisions, and other qualifying instruments. Tier 2 cannot exceed Tier 1 capital.

Capital Conservation Buffer and Countercyclical Buffer

Beyond the minimum CRAR, Basel III introduced additional capital buffers that Indian banks must maintain:

Capital Conservation Buffer (CCB): An additional 2.5 percent of RWAs, composed entirely of CET1, which banks must hold above the minimum requirement. Failure to maintain this buffer restricts dividend payouts, share buybacks, and discretionary bonus payments. This brings the effective minimum CET1 requirement for Indian banks to 8 percent.

Countercyclical Capital Buffer (CCyB): A variable buffer that the RBI can activate during periods of excessive credit growth, requiring banks to hold additional CET1 of up to 2.5 percent. As of the latest RBI guidance, the CCyB for Indian banks remains at zero percent, though its activation framework is in place.

D-SIB Surcharge: Domestic Systemically Important Banks (D-SIBs) — currently SBI, HDFC Bank, and ICICI Bank — are required to hold an additional CET1 surcharge ranging from 0.2 to 0.8 percent depending on their systemic importance bucket, to reflect the heightened risks they pose to the financial system.

Risk-Weighted Assets: The Denominator That Matters

The CRAR ratio is only as meaningful as the accuracy of the risk weights applied to assets. The RBI prescribes standardised risk weights for various asset classes: zero percent for sovereign exposures, 20 percent for claims on scheduled banks, 75 percent for qualifying retail exposures, 100 percent for corporate loans, 150 percent or higher for certain stressed or speculative exposures, and so on. Banks using the Internal Ratings-Based (IRB) approach — not yet widely permitted in India — can use their own models under supervisory approval.

The Investment Fluctuation Reserve: A Buffer Now Scrapped

Until recently, the RBI required banks to build an Investment Fluctuation Reserve (IFR) — a dedicated buffer to cushion mark-to-market losses on their held-for-trading and available-for-sale investment portfolios when interest rates rose. In a significant policy shift, the RBI has decided to do away with the IFR requirement, recognising that the shift to the new investment classification and valuation norms under the revised framework (which introduced three categories: Held to Maturity, Available for Sale, and Fair Value Through Profit or Loss) already embeds market risk recognition more systematically. This move is expected to release capital that banks had earmarked for the IFR, providing a meaningful boost to their available capital resources.

Additionally, the RBI has signalled its intent to relax NPA-linked capital rules and ease restrictions on the inclusion of profits in regulatory capital calculations. These changes collectively represent a calibrated loosening of capital constraints, aimed at enabling banks to lend more aggressively to support economic growth without compromising systemic safety.

How NBFC Capital Requirements Differ from Bank Norms

The NBFC Landscape: A Heterogeneous Universe

Unlike the relatively homogeneous world of scheduled commercial banks, the NBFC sector is extraordinarily diverse. It encompasses asset finance companies, loan companies, investment companies, infrastructure finance companies, housing finance companies (regulated by the National Housing Bank), microfinance institutions, account aggregators, peer-to-peer lending platforms, and more. This diversity means that the capital framework for NBFCs cannot be a simple replica of the bank framework.

Net Owned Fund: The Starting Point

The most fundamental capital requirement for NBFCs is the maintenance of a minimum Net Owned Fund (NOF). The NOF is essentially the paid-up equity capital plus free reserves, minus accumulated losses, deferred revenue expenditure, and other intangible assets. Following a phased revision, the RBI has progressively raised the minimum NOF threshold:

For most deposit-taking and non-deposit-taking NBFCs in the upper and middle layers: the minimum NOF is now ₹10 crore, raised from the earlier ₹2 crore threshold.

For NBFCs in the Base Layer (smaller, less systemically significant entities): a lower threshold may apply, subject to specific category rules.

CRAR for NBFCs: A Lower but Evolving Bar

NBFCs are required to maintain a CRAR, but the computation and the minimum threshold differ from banks:

Non-deposit-taking NBFCs with asset size above ₹500 crore (NBFC-ND-SI) and all deposit-taking NBFCs are required to maintain a minimum CRAR of 15 percent, which is higher than the 9 percent prescribed for banks. This might appear counterintuitive, but it reflects the fact that NBFCs do not have access to low-cost, insured retail deposits, carry higher refinancing risk, and have less diversified funding bases.

The composition of NBFC capital under the RBI's Scale Based Regulation (SBR) framework — introduced in 2021 and fully implemented in a phased manner — increasingly mirrors Basel III terminology, with Tier 1 and Tier 2 categories defined for qualifying instruments.

For Infrastructure Finance Companies (IFC-NBFCs), the minimum CRAR is set at 15 percent, with at least 10 percent in Tier 1 capital, reflecting the long-tenor, illiquid nature of infrastructure assets.

Microfinance NBFCs (NBFC-MFIs) have distinct capital norms aligned with their social mandate and rural lending focus.

Leverage Ratio and Concentration Norms

In addition to CRAR, the RBI imposes leverage limits on NBFCs — particularly the stipulation that their total outside liabilities should not exceed a certain multiple of their NOF. For most NBFC-ND-SIs, the leverage ratio is capped at 7 times the NOF, though this has been relaxed for certain infrastructure-focused entities. Banks, by contrast, are subject to the Basel III leverage ratio framework (minimum 3 percent under Basel III), with the RBI applying a stricter 4 percent floor for D-SIBs.

Provisioning as a Quasi-Capital Tool

NBFCs are also required to make standard asset provisioning — a requirement that, while technically an income statement item, effectively builds a quasi-capital buffer against future credit losses. The provisioning norms for NBFCs have been progressively harmonised with bank norms under the SBR framework, though some differences in the classification timelines for NPAs persist.

RBI's Move to Align Bank and NBFC Capital Rules: Implications

The Scale Based Regulation Framework: A Convergence Agenda

The RBI's SBR framework, operationalised from October 2022 onwards, represents the most ambitious attempt to bring NBFC regulation closer to bank-equivalent standards for larger, systemically important entities. Under SBR, NBFCs are categorised into four layers:

Base Layer (NBFC-BL): Smaller NBFCs with lower systemic risk, subject to lighter-touch regulation.

Middle Layer (NBFC-ML): Deposit-taking NBFCs, non-deposit-taking NBFCs above ₹1,000 crore in assets, and certain specialised categories. Subject to enhanced capital and governance norms.

Upper Layer (NBFC-UL): The top 10 NBFCs identified by the RBI on the basis of size, interconnectedness, and systemic importance. These entities are subject to near-bank levels of regulation, including enhanced CRAR requirements, leverage norms, and corporate governance standards. The RBI has the authority to require Upper Layer NBFCs to list on recognised stock exchanges within three years of being classified as such.

Top Layer (NBFC-TL): A reserve category that would be populated only if the RBI determines that specific NBFCs pose exceptional systemic risk, warranting conversion to bank status.

Easing Capital Norms for Banks: Strategic Timing

The recent RBI decisions to scrap the IFR requirement, ease NPA-linked capital rules, and relax profit inclusion norms for banks come at a strategic juncture. With India targeting GDP growth above 7 percent, banks need room to expand credit without being constrained by capital buffers that regulators now view as redundant or duplicative. The relaxation of the IFR is particularly notable: it removes a layer of conservatism that, while prudent during periods of interest rate volatility, may no longer be necessary given the new investment classification framework.

For NBFCs, the implications are subtler. As bank capital is freed up and banks can lend more competitively, NBFCs — particularly those in the middle and upper layers — may face stiffer competition for prime corporate and retail borrowers. However, NBFCs retain an edge in niche segments: vehicle finance, gold loans, microfinance, and last-mile rural credit, where their operational models are more agile than traditional bank branches.

Widening Market Access: Primary Dealers and Term Money

The RBI's decision to widen term money market access and raise borrowing limits for primary dealers is relevant to the capital adequacy discussion because it affects liquidity management — a close cousin of capital management. Primary dealers, many of which are subsidiaries of large banks or NBFCs, can now access term funds more easily, reducing rollover risk and improving their ability to hold government securities without the volatility concerns that previously necessitated the IFR. This systemic liquidity improvement complements the capital easing measures.

What Regulatory Convergence Means for the Industry

The gradual convergence of bank and NBFC capital norms has important implications across the financial ecosystem:

For investors: Upper Layer NBFCs facing bank-equivalent capital requirements may need to raise equity capital through rights issues, qualified institutional placements, or public listings, creating investment opportunities but also dilution risks for existing shareholders.

For borrowers: A better-capitalised NBFC sector is a more resilient one. Borrowers — particularly in the MSME and retail segments — benefit from NBFCs that can absorb shocks without abruptly tightening credit.

For regulators: Convergence simplifies supervisory comparisons and reduces the scope for regulatory arbitrage, where entities structure themselves as NBFCs primarily to avoid stricter bank capital rules.

For the credit cycle: Capital adequacy norms are procyclical by nature — they tend to constrain lending during downturns when capital is scarce. The RBI's CCyB framework and the easing of certain bank capital rules are attempts to manage this procyclicality intelligently.

Conclusion: Capital Adequacy as a Living Framework

The comparison of bank vs NBFC capital adequacy norms in India reveals a system in deliberate transition — one that is moving from a historically bifurcated regulatory architecture toward a more risk-proportionate, convergent framework. Banks operate under a sophisticated Basel III-aligned regime with CRAR, capital buffers, and D-SIB surcharges that are globally benchmarked. NBFCs, while subject to a higher headline CRAR of 15 percent, have operated with less granular buffer requirements and greater flexibility — a gap that the SBR framework is systematically narrowing for larger, systemically connected entities.

The RBI's recent capital relaxations for banks — scrapping the IFR, easing NPA-linked capital rules, and liberalising profit inclusion norms — reflect a mature regulator's ability to calibrate requirements dynamically, removing buffers that have served their purpose while retaining those that address genuine systemic vulnerabilities. For NBFC practitioners, board members, and investors, the message from the regulatory direction is clear: scale brings scrutiny, and the closer an NBFC's footprint resembles a bank's, the more its capital regime will look like one.

Staying abreast of these evolving norms is not optional for finance professionals operating in India's credit markets — it is foundational to sound risk management, strategic capital planning, and regulatory compliance in an increasingly dynamic financial landscape.