IBC Insolvency Resolution Process in India: A Comprehensive Guide

The insolvency resolution process in India under IBC has fundamentally transformed how distressed assets and financially troubled companies are handled across the country. Before the Insolvency and Bankruptcy Code (IBC) came into force in 2016, creditors — particularly banks — were left chasing defaulters through a maze of overlapping legislation, including the SARFAESI Act, the Sick Industrial Companies Act (SICA), and the Recovery of Debts Due to Banks and Financial Institutions Act. Recovery was slow, haircuts were steep, and the moral hazard for promoters was significant. The IBC changed the equation by consolidating the insolvency framework, introducing strict timelines, and shifting the balance of power decisively in favour of creditors. Today, as policymakers debate a proposed creditor-led resolution framework to make the process even faster, understanding the architecture of the current system has never been more relevant for Indian banking professionals, legal practitioners, and investors.

What Is the Insolvency and Bankruptcy Code (IBC) 2016?

The Insolvency and Bankruptcy Code, 2016 is a landmark piece of legislation that provides a consolidated and time-bound framework for resolving insolvency and bankruptcy in India. It covers individuals, partnership firms, limited liability partnerships (LLPs), and corporate persons. The Code was enacted to address a critical gap: India's gross non-performing assets (NPAs) had swelled to alarming levels, and the existing recovery mechanisms were neither fast nor effective.

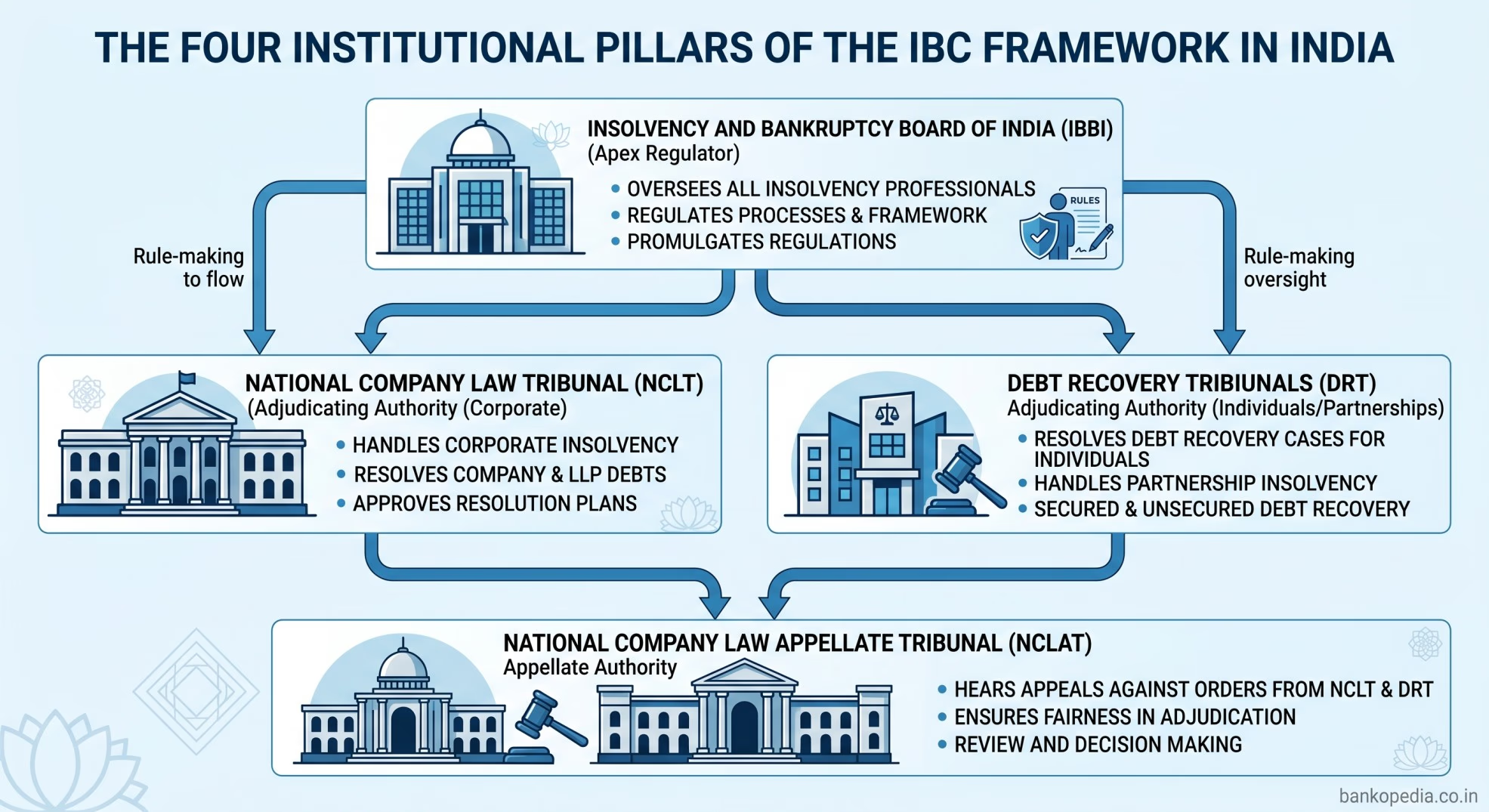

The IBC is administered through several key institutional pillars:

Insolvency and Bankruptcy Board of India (IBBI): The apex regulatory body that oversees insolvency professionals, insolvency professional agencies, information utilities, and the overall functioning of the Code.

National Company Law Tribunal (NCLT): The adjudicating authority for corporate insolvency and bankruptcy.

National Company Law Appellate Tribunal (NCLAT): The appellate body for orders passed by NCLT.

Debt Recovery Tribunals (DRTs): The adjudicating authority for individual and partnership insolvency cases.

The Code introduced the concept of a default-triggered process: any creditor (financial or operational) or even the corporate debtor itself can initiate insolvency proceedings upon a default of at least ₹1 crore (the threshold was raised from ₹1 lakh to ₹1 crore during the COVID-19 pandemic period). This single shift — from a debtor-in-possession model to a creditor-in-control model — is arguably the most significant structural reform in Indian credit markets in decades.

The RBI has been an active stakeholder in the IBC ecosystem, particularly through its Prudential Framework for Resolution of Stressed Assets (June 2019), which encouraged banks to proactively identify stress and initiate resolution before accounts slid into formal insolvency. SEBI has also engaged with IBC processes, particularly in cases involving listed corporate debtors where disclosures and market-sensitive information need careful handling during the Corporate Insolvency Resolution Process (CIRP).

"The IBC has shifted the fulcrum from debtor protection to creditor rights, instilling a credit discipline that was sorely missing in the Indian financial ecosystem."

Step-by-Step: How the Corporate Insolvency Resolution Process (CIRP) Works

The Corporate Insolvency Resolution Process (CIRP) is the most frequently used mechanism under the IBC, applicable to companies and LLPs. Here is a structured breakdown of how the process unfolds from initiation to resolution:

Step 1: Filing an Application with NCLT

A CIRP can be initiated by a financial creditor (such as a bank or non-banking financial company), an operational creditor (such as a vendor or employee), or the corporate debtor itself. The application must establish a debt and a default. For financial creditors, this process is relatively straightforward; for operational creditors, there is an additional requirement to issue a demand notice before filing.

Step 2: Admission and Appointment of Interim Resolution Professional (IRP)

Once the NCLT is satisfied that a default has occurred, it admits the application — ideally within 14 days of filing — and declares a moratorium. This moratorium is critical: it prohibits the institution or continuation of suits against the corporate debtor, prevents transfer or disposal of assets, and halts recovery actions. Simultaneously, an Interim Resolution Professional (IRP) is appointed to manage the affairs of the company during this period.

Step 3: Formation of the Committee of Creditors (CoC)

Within 30 days of appointment, the IRP must constitute a Committee of Creditors (CoC), comprising all financial creditors of the corporate debtor. Voting rights within the CoC are proportional to the financial debt owed. Operational creditors above a threshold may attend CoC meetings but do not have voting rights. The CoC is the supreme decision-making body during CIRP — it can either replace the IRP with a Resolution Professional (RP) of its choosing or ratify the IRP's continuation.

Step 4: Resolution Professional Takes Over

The Resolution Professional (RP) assumes control of the corporate debtor, displacing the erstwhile management. The RP is responsible for managing day-to-day operations, collating all claims from creditors, preparing an Information Memorandum (IM), and inviting resolution plans from prospective resolution applicants. The RP also has the power to identify and challenge preferential, undervalued, fraudulent, or extortionate transactions that may have been entered into by the company prior to insolvency.

Step 5: Invitation and Evaluation of Resolution Plans

The RP issues a Request for Resolution Plans (RFRP) to prospective applicants who meet the IBBI's eligibility criteria. Crucially, Section 29A of the IBC bars promoters and connected parties responsible for the default from submitting resolution plans, subject to certain exceptions. Resolution applicants submit detailed plans covering how they intend to revive the company, settle creditor dues, and ensure continued operations.

Step 6: Approval by CoC and NCLT

The CoC evaluates competing resolution plans using a defined evaluation matrix and approves a plan by a 66% majority vote. The approved plan is then submitted to NCLT for judicial sanctioning. NCLT examines whether the plan complies with the requirements of the IBC and does not contravene any law before passing its order. Once sanctioned, the plan is binding on all stakeholders — creditors, shareholders, employees, and government authorities.

Step 7: Liquidation (If No Resolution Plan Is Approved)

If no viable resolution plan is received or approved within the statutory timeline, the NCLT orders liquidation of the corporate debtor. The proceeds are distributed in a strict statutory waterfall: insolvency resolution costs first, then secured creditors and workmen's dues, followed by other employee dues, unsecured creditors, government dues, and finally, equity shareholders.

The IBC mandates completion of CIRP within 180 days, extendable by 90 days with CoC approval, and subject to a hard deadline of 330 days including litigation time. In practice, however, delays have been significant, with many cases breaching the 330-day mark due to judicial capacity constraints and complex litigation.

Role of Creditors, Resolution Professionals, and NCLT

The IBC's effectiveness hinges on the interplay between three critical actors: creditors (particularly through the CoC), Resolution Professionals, and the NCLT. Each plays a distinct but interdependent role.

Financial Creditors and the Committee of Creditors

Banks and financial institutions dominate the CoC in most large corporate insolvency cases. Institutions such as State Bank of India, Punjab National Bank, HDFC Bank, ICICI Bank, and others regularly participate as major CoC members in high-value CIRPs. The CoC is vested with commercial wisdom — a concept that the Supreme Court of India has repeatedly affirmed, cautioning tribunals against substituting their judgment for that of the CoC on commercial decisions.

However, the CoC's conduct is not beyond scrutiny. Operational creditors have raised concerns about being systematically under-compensated in resolution plans. The Supreme Court, in the landmark Committee of Creditors of Essar Steel v. Satish Kumar Gupta (2019), clarified that while the CoC has overriding commercial wisdom, the resolution plan must pay attention to the dues of operational creditors in a fair and equitable manner.

Resolution Professionals

The RP is the engine of the CIRP. Registered with one of the IBBI-recognised Insolvency Professional Agencies (IPAs), the RP must balance fiduciary obligations to the CoC with statutory duties toward all creditors, employees, and the integrity of the process. The IBBI has progressively tightened its oversight of IPs, mandating continuing professional education, imposing penalties for misconduct, and publishing inspection reports to ensure accountability.

One persistent challenge is the availability and capacity of qualified insolvency professionals for large, complex cases involving thousands of creditors and multistate operations. The IBBI's data consistently shows that a small cohort of experienced IPs handles a disproportionately large share of significant cases.

NCLT: Adjudicating Authority

The NCLT plays a dual role — it admits applications and sanctifies outcomes, but it must refrain from micromanaging the commercial aspects of the resolution process. With 16 benches across India, NCLT has been stretched by the sheer volume of IBC filings. Pendency of cases and delays in admission, as well as in hearing liquidation proceedings, remain structural challenges. Judicial appointments and infrastructural upgrades to NCLT benches remain ongoing priorities for the Ministry of Corporate Affairs.

Proposed Creditor-Led Resolution Framework: What Could Change?

In a significant policy development, policymakers and industry stakeholders have been actively deliberating a creditor-led resolution framework that could operate outside the formal NCLT-supervised CIRP. The proposal, which has gained fresh momentum in recent discussions, seeks to address one of the IBC's most persistent criticisms: delays that erode asset value and increase haircuts for creditors.

The Core Idea

Under the proposed framework, creditors — led by the CoC — would be empowered to drive the resolution process with significantly reduced judicial supervision. Rather than routing every procedural step through NCLT, the CoC would negotiate directly with resolution applicants, approve a plan, and seek only final judicial approval. This mirrors models used in certain other jurisdictions, including the UK's scheme of arrangement process and elements of the US Chapter 11 bankruptcy framework.

Key Proposed Features

Pre-packaged insolvency mechanism extension: The IBC already introduced a pre-packaged insolvency resolution process (PIRP) for Micro, Small and Medium Enterprises (MSMEs) in 2021. The proposed framework would extend a similar philosophy — where a resolution plan is negotiated prior to formal NCLT filing — to larger corporates.

Reduced timeline: Proponents argue that a creditor-led framework could compress resolution timelines significantly, potentially to under 90 days in straightforward cases, thereby preserving going concern value.

Greater role for RBI and sectoral regulators: In cases involving regulated entities (banks, NBFCs, insurance companies), the RBI and IRDAI would likely play an enhanced supervisory role in validating the integrity of creditor-led processes before NCLT sanction.

Moratorium and interim protections: Any creditor-led framework would need to retain robust protections against asset stripping during the resolution period, a concern that SEBI has also flagged in the context of listed companies where minority shareholders can be adversely affected.

Concerns and Counterarguments

Not all stakeholders are enthusiastic. Operational creditors, smaller financial creditors, and employee unions have raised concerns that a creditor-dominated framework could marginalise their interests further. There is also a systemic risk argument: removing judicial oversight too early in the process could create opportunities for collusion between dominant creditors and resolution applicants, particularly in cases involving related parties.

Bankers themselves have begun tightening internal processes in parallel — a trend captured by recent reports of banks demanding comprehensive documentation from borrowers to guard against potential FEMA (Foreign Exchange Management Act) violations and related regulatory fallout. This heightened compliance posture underscores the fact that insolvency proceedings can open up a company's entire transaction history to scrutiny, making pre-CIRP hygiene increasingly important.

The creditor-led framework is not about removing accountability — it is about relocating the centre of gravity from the courtroom to the boardroom of lenders, while maintaining sufficient guardrails for fair play.

Legislative Path Forward

Implementing a creditor-led framework of this nature would require amendments to the IBC, potentially new IBBI regulations, and possibly coordination with RBI's prudential norms governing how banks classify and provision accounts undergoing such processes. The Ministry of Corporate Affairs and the IBBI have been known to consult extensively before amending the Code — a process that, while sometimes slow, has produced well-calibrated reforms such as the Section 29A amendments and the MSME PIRP.

Conclusion: Building a More Efficient Insolvency Ecosystem

The insolvency resolution process in India under IBC has, in less than a decade, recovered over ₹3.16 lakh crore for creditors (as per IBBI data) and resolved hundreds of large corporate defaults that would have remained festering under earlier frameworks. Yet the system is not without its challenges — delays, high haircuts, CoC dominance concerns, and the growing backlog at NCLT tribunals continue to demand attention.

The proposed creditor-led resolution framework represents the next logical evolution: a mechanism that retains the structural strengths of the IBC while reducing process friction. For Indian banking professionals, the message is clear — understanding the granular mechanics of CIRP, from the moratorium and CoC formation to RP obligations and resolution plan evaluation, is no longer optional knowledge. It is a core competency.

As India's credit markets deepen, as new asset classes (infrastructure debt, real estate, green finance) create novel insolvency scenarios, and as cross-border insolvency issues gain prominence, the IBC framework will continue to evolve. Staying informed about these changes — and contributing meaningfully to policy consultations — is how India's banking community can help shape a truly world-class insolvency architecture.

For more in-depth analysis of IBC developments, NCLT judgments, and banking regulation updates, stay connected with Bankopedia — your trusted source for Indian banking and finance knowledge.