The Macroeconomic Context: How GST Affects Affordability

The relationship between GST on health insurance premiums and actual market affordability is far more layered than a simple percentage calculation suggests. To understand the friction, one must look at India's insurance penetration metrics. Insurance penetration — defined as total premium income as a percentage of the Gross Domestic Product (GDP) — stood at approximately 4% in recent years, with health insurance contributing only a fraction of that figure. Compare this to developed economies, or even peer emerging markets, where insurance penetration regularly crosses 8–12%, and the gap becomes stark.

Taxation is certainly not the sole reason for low penetration; lack of awareness, complex underwriting, and historical reliance on out-of-pocket expenditure (OOPE) play massive roles. However, taxation is a highly measurable, immediate deterrent. India’s OOPE for health remains stubbornly high, forcing millions into poverty every year due to catastrophic medical events.

Consider the behavioural economics at play. A first-time health insurance buyer in a Tier 2 or Tier 3 city is already navigating a severe trust deficit around insurance products. They are worried about complex policy wordings, hidden sub-limits, co-payments, and the overarching fear of claim rejections at the point of care. When this hesitant buyer discovers that nearly one-fifth of their hard-earned money is going toward government tax rather than actual medical coverage, the psychological impact on their purchase decision is non-trivial.

Financial literacy research and consumer elasticity studies consistently show that opaque or seemingly punitive taxation on welfare-oriented products significantly reduces market uptake, particularly among lower-middle-income groups who are highly price-sensitive. For this demographic, a ₹2,000 difference in premium is often the deciding factor between buying a policy and hoping for the best without one.

The Senior Citizen Problem: A Tax on Aging

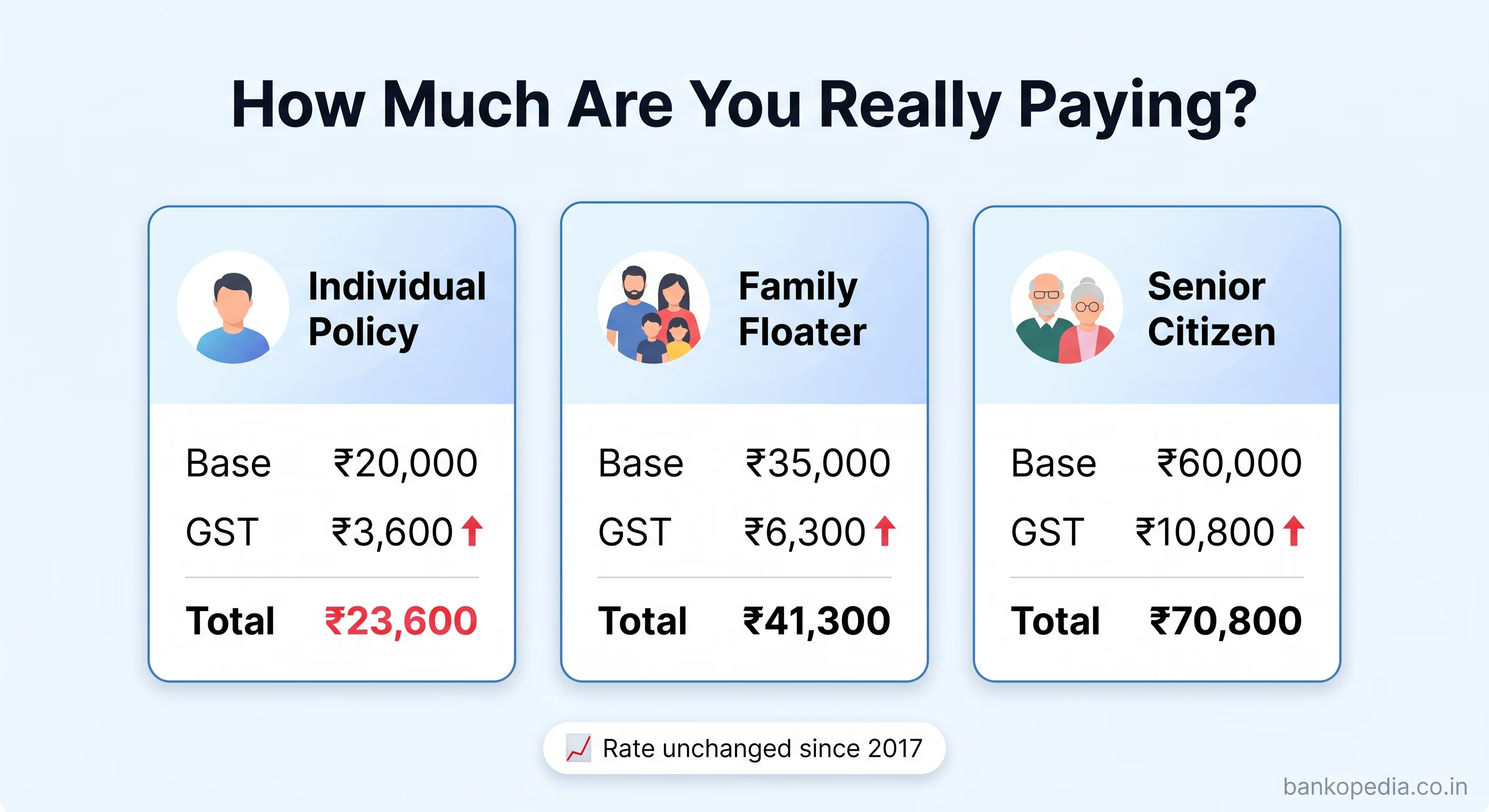

The issue of high taxation is most acute and financially devastating for senior citizens. As individuals cross the age of 60, their risk profile changes dramatically in the eyes of actuaries. Base premium rates for individuals above 60 years of age can range from ₹25,000 to well over ₹80,000 annually, depending heavily on the sum insured, geographical zone, pre-existing conditions (like hypertension or diabetes), and the specific insurer's risk appetite.

At 18% GST, a senior citizen paying ₹60,000 in an annual base premium is handing over an additional ₹10,800 in tax alone. For retirees living on fixed incomes — such as pensions, interest from fixed deposits, or modest rental income — this is a substantial and recurring outflow that compounds every year as premiums naturally rise with age bands.

The legislature has taken note of this structural flaw. A parliamentary standing committee on finance had explicitly noted in its reports that the 18% GST on health and life insurance premiums is "irrational and contradictory to the government's objective of increasing insurance penetration."

The committee recommended either full exemption or at least a drastic reduction to 5% for health insurance products, with a specific emphasis on easing the burden for the elderly. The fact that such a strongly worded recommendation emerged from a cross-party parliamentary body reflects how broadly the concern is shared across the political spectrum. Taxing the healthcare safety net of the elderly at the same rate as luxury consumption is increasingly viewed as an untenable policy stance.

Factual Correction: The Strict Nuances of Input Tax Credit (ITC)

A common misconception in corporate finance and among MSMEs is that businesses purchasing group health insurance for their employees can seamlessly claim Input Tax Credit (ITC) to offset their GST liabilities. It is vital to factually correct this notion.

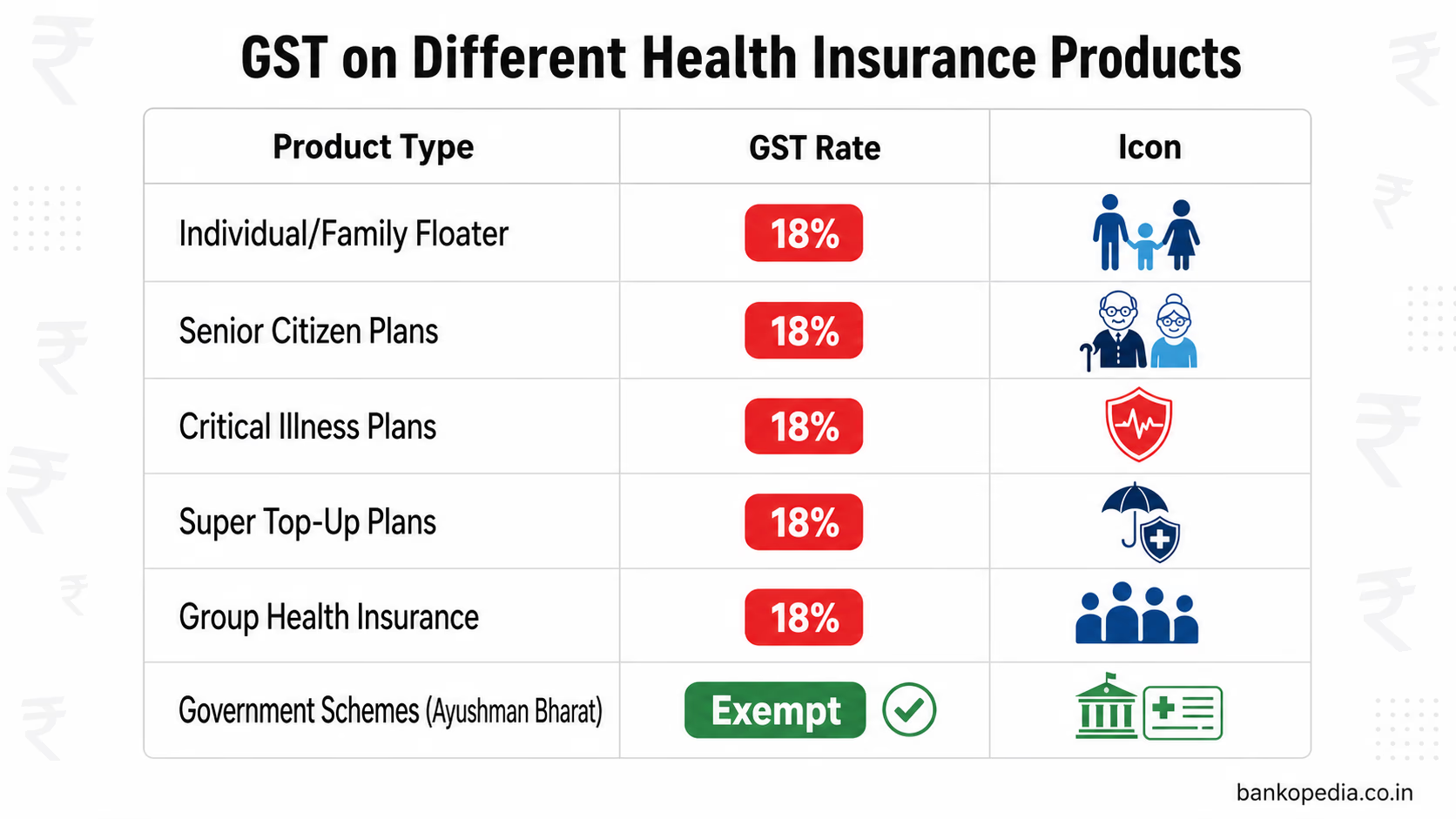

Under the Central Goods and Services Tax (CGST) Act, specifically Section 17(5)(b)(iii)(A), the law explicitly blocks the availability of Input Tax Credit on health insurance, life insurance, and maternity benefits.

There is only one major exception: a business can claim ITC on employee health insurance only if the provision of such insurance is strictly mandated by an applicable law under which the business operates. For example, during the COVID-19 pandemic, specific Ministry of Home Affairs guidelines temporarily mandated employers to provide health cover, allowing a brief window of ITC applicability. Similarly, certain provisions under the Factories Act might mandate specific health covers for hazardous roles.

However, for the vast majority of standard IT companies, service sector firms, startups, and general corporate employers offering group mediclaim as an employee retention benefit or HR perk, no Input Tax Credit is available.

The 18% GST paid on corporate group health policies is a "sticky" cost that goes straight to the company's profit and loss statement as an expense. This lack of ITC makes providing comprehensive health benefits significantly more expensive for employers, indirectly discouraging MSMEs and smaller startups from offering robust health covers to their workforce. Furthermore, individual policyholders — the retail segment — naturally receive no such relief, making the system universally expensive.

The Income Tax Mirage: Section 80D vs. The New Tax Regime

Historically, financial advisors have pointed to the Income Tax Act as a way to soften the blow of GST. Section 80D allows taxpayers to claim deductions on health insurance premiums paid for themselves, their families, and dependent parents. The limits are up to ₹25,000 for individuals and up to ₹50,000 for senior citizens.

However, this argument requires a major factual update based on recent macroeconomic shifts in India's taxation policy. The government has aggressively repositioned the New Tax Regime as the default and more mathematically beneficial option for the vast majority of the salaried middle class.

The critical feature of the New Tax Regime is the deliberate removal of almost all Chapter VI-A deductions, including Section 80D. As millions of Indian taxpayers migrate to the New Tax Regime to benefit from lower base slab rates and higher rebate limits, they completely lose the ability to offset their health insurance premiums against their taxable income.

For a taxpayer under the New Regime, the 18% GST on health insurance is no longer partially subsidized by an income tax refund; it is a 100% deadweight out-of-pocket cost. This paradigm shift makes the argument for reducing the GST rate at the source exponentially more urgent. The old mechanism of giving with one hand (80D) while taking with the other (18% GST) is rapidly disappearing, leaving only the heavy taxation.

"The effective cost of health insurance in India, when GST is factored in alongside rising medical inflation, makes it one of the most expensive risk mitigation instruments for the average Indian household relative to income levels."

The Compound Burden: GST and Medical Inflation

To truly understand the weight of the GST burden, it must be viewed in tandem with medical inflation. India's medical inflation rate consistently hovers between 12% to 15% annually, heavily outpacing standard retail inflation (CPI).

When a hospital increases its room rents, surgical fees, and consumable charges, insurance companies experience higher claim severities. To maintain their solvency margins and combined ratios, insurers must inevitably hike their base premiums.

Because GST is applied as a percentage (18%) on the base premium, the tax amount scales linearly with medical inflation. If an insurer raises a family floater premium from ₹30,000 to ₹35,000 due to inflation, the government's tax collection automatically jumps from ₹5,400 to ₹6,300 without any change in the tax policy itself. This creates a compounding effect where policyholders are penalized twice: once by the rising cost of private healthcare, and second by the proportionately rising indirect tax.

Standalone Health Insurers vs. General Insurers: The Mechanics of Reform

The Indian health insurance market is served by two broad categories of insurers: Standalone Health Insurance Companies (SAHIs), which exclusively offer health and allied products, and General Insurance Companies (Non-Life), which offer health insurance alongside motor, fire, marine, property, and liability covers. Understanding the operational distinction between these entities is essential when evaluating the potential market impact of any GST reform.

The SAHI Advantage in a GST-Cut Scenario

Standalone health insurers — a list that includes prominent names like Star Health and Allied Insurance, Niva Bupa Health Insurance, Care Health Insurance, and Aditya Birla Health Insurance — have built their entire operational infrastructure around health products. Their product innovation, distribution networks (including massive agency forces), hospital network management, and customer communication channels are all strictly optimised for the healthcare consumer.

In a scenario where the GST Council reduces the rate — say, to 5% or zero-rates it for specific demographics — SAHIs are positioned to benefit disproportionately. Here is the economic breakdown of why:

Price Sensitivity and Volume Growth: SAHIs operate in a highly elastic segment of the retail market. Individual and family health insurance buyers are notoriously price-sensitive. A meaningful GST reduction from 18% to 5% would immediately make the final checkout price significantly cheaper. Basic price elasticity of demand dictates that this drop in price would trigger higher sales volumes, pulling fence-sitters into the insured pool.

Premium Reinvestment and Product Enhancement: If the tax burden drops, SAHIs have the pricing headroom to innovate. They could choose to pass the entire 13% savings directly to the consumer, or they could keep the total checkout price similar but drastically enhance the base product — offering a higher sum insured, removing room rent sub-limits, offering day-1 cover for certain diseases, or reducing waiting periods for pre-existing conditions.

Penetration into Underserved Geographies: SAHIs have been aggressively targeting Tier 2, Tier 3, and Tier 4 cities through digital channels and bancassurance. In these markets, absolute affordability is the single largest barrier. A tax cut amplifies their ability to convert prospects into active policyholders, thereby fulfilling the regulator's mandate of deeper rural and semi-urban penetration.

General Insurers: Diversified but Less Responsive

General insurers, including massive public sector behemoths like New India Assurance, Oriental Insurance, National Insurance, and United India Insurance, alongside large private players like ICICI Lombard and Bajaj Allianz, treat health insurance as just one vertical in a vast diversified portfolio.

For these companies, a GST cut on health insurance would certainly benefit their health portfolios, but it would not fundamentally transform their overall business economics as dramatically as it would for SAHIs. Their revenues from mandatory motor third-party insurance or massive corporate fire policies often overshadow retail health.

Furthermore, public sector general insurers, which still dominate certain regional markets due to historical trust and vast institutional scale, are often burdened by legacy pricing structures, high incurred claim ratios in health, and bureaucratic processes. They might be mechanically slower in passing on the immediate benefits of a GST reduction to consumers. The IRDAI would likely need to step in with strict, clear guidelines mandating how premium pricing tables must be instantly revised to reflect any GST rate reductions, ensuring the benefit reaches the end consumer rather than being absorbed into corporate margins.

The Reinsurance Dimension

When discussing the taxation of insurance, the back-end architecture of the industry is frequently overlooked. It is vital to note that reinsurance premiums — the insurance that insurance companies buy to protect their own balance sheets — also attract GST.

When an Indian insurer cedes a portion of its risk to a foreign reinsurer, GST is applicable under the Reverse Charge Mechanism (RCM). This means the Indian insurer is liable to pay the GST to the government on behalf of the foreign reinsurer. Even domestic arrangements with entities like GIC Re (India's national reinsurer) involve GST calculations.

This adds a hidden layer of embedded cost to the overall health insurance ecosystem. While insurers can generally claim input credits against their output liabilities in these specific B2B transactions, the working capital blockages and compliance overheads create friction. Any genuine, holistic rationalisation of GST on health insurance would ideally need to evaluate the entire value chain, from the retail policyholder all the way up to global reinsurance treaties, to guarantee a lasting reduction in consumer premiums.

History of GST Reform Demands and Recent GoM Developments

The demand to reduce or eliminate GST on health insurance premiums is not a new phenomenon; it has been consistently raised by industry bodies, consumer advocacy groups, and lawmakers since the exact moment GST was rolled out in 2017.

Timeline of Key Demands and Deliberations

2019–2020: The Life Insurance Council and the General Insurance Council separately submitted exhaustive representations to the Ministry of Finance. Their core argument was ideological as much as economic: insurance is a social good, a pillar of public welfare, and should not be taxed alongside luxury consumption. They requested a blanket reduction to 5%.

2021: The Parliamentary Standing Committee on Finance, in its comprehensive report on the insurance sector, formally recommended exempting term life insurance and health insurance from GST, labelling the 18% rate as "counterproductive" to national financial security.

2023: During pre-Budget consultations, the IRDAI reiterated to the Finance Ministry that high taxation is a primary structural barrier to achieving its ambitious "Insurance for All by 2047" vision.

2024–2025 The Turning Point: The debate reached a crescendo. Facing immense pressure from the opposition, the middle class, and industry leaders, the GST Council formally constituted a Group of Ministers (GoM) specifically tasked with reviewing the taxation of life and health insurance. Extensive deliberations took place, focusing heavily on the political and social cost of taxing senior citizens. Reports emerging from these high-level meetings indicated a strong consensus building toward entirely exempting (zero-rating) health insurance premiums for senior citizens, and potentially introducing a lower 5% slab for individuals holding basic coverage up to ₹5 lakh.

Despite these persistent pushes, the ultimate decision rests on fiscal mathematics. The GST Council operates on consensus between the Centre and the states. States, historically wary of revenue foregone (especially post the end of the GST compensation period), have been reluctant to slash a steady revenue stream. Health and life insurance combined yield tens of thousands of crores in GST collections annually. A rate cut requires a compensatory mechanism or a leap of faith that volume growth will offset the immediate revenue loss.

What a GST Rate Cut Would Look Like in Practice

If the GST Council were to officially notify a reduction in the rate on retail health insurance to 5%, the immediate mathematical relief would be palpable. The annual savings for a family paying ₹20,000 in base premium would be ₹2,600 — the absolute difference between ₹3,600 (tax at 18%) and ₹1,000 (tax at 5%).

While saving ₹2,600 may appear modest in isolation, when scaled across India's approximately 50 crore health insurance policyholders (spanning retail, group, and mass segments), the aggregate macroeconomic demand stimulus is massive. Actuaries and insurance economists argue strongly that the induced volume growth from these premium savings would partially, if not entirely, offset the aggregate revenue loss to the government over a 3-to-5-year horizon.

More importantly, a larger insured population dramatically reduces the long-term fiscal burden on public health infrastructure. Every citizen who utilizes private insurance for a surgery is one less citizen relying on heavily subsidized, overcrowded government hospitals. The government saves money on public healthcare delivery when private insurance penetration rises.

The Road Ahead: IRDAI's Regulatory Push and GST Council's Agenda

The IRDAI’s current regulatory posture is one of aggressive modernization. Initiatives like the "Bima Trinity" (Bima Sugam, Bima Vahak, and Bima Vistaar), allowing use-and-file product launches, expanding bancassurance tie-ups, and proposing composite insurance licences all signal a systemic, aggressive push to broaden the insured base.

However, regulatory liberalisation alone cannot solve the core affordability problem if the overarching tax structure remains rigid. The most credible, fiscally prudent near-term pathway to GST reform on health insurance involves a tiered, nuanced approach:

Zero GST for all senior citizen health insurance policies.

A reduced rate of 5% for basic individual and family floater policies below a certain sum insured threshold (e.g., ₹5 lakh or ₹10 lakh).

Retaining the 18% rate strictly for ultra-high-net-worth policies, global coverage plans, or super top-ups exceeding ₹50 lakh.

This calibrated approach would carefully protect the fiscal revenues of both the Centre and the States while directly, surgically delivering relief to the mass market segment that needs the most state support. With the government's stated ambition of expanding social security coverage and driving the "Viksit Bharat 2047" agenda, there is clear ideological alignment for reducing tax friction. The political will, navigating the complex centre-state fiscal relations, remains the final variable.

Practical Takeaways for Policyholders and Finance Professionals

While the policy debate continues in the halls of the GST Council, there are several practical, actionable steps that individual policyholders and financial professionals can implement within the current rigid 18% framework:

Evaluate Tax Regimes Carefully: Before defaulting to the New Tax Regime, mathematically compare your total tax outflow. If you are paying high premiums for yourself and senior citizen parents, the Section 80D benefits under the Old Tax Regime might still offer better net savings, offsetting the GST burden.

Corporate HR and ITC Awareness: Employers must be fully aware that standard health insurance does not attract ITC under Section 17(5). Budget allocations for employee benefits must account for the 18% as a sunk cost, avoiding compliance errors in GST filings.

Compare on a Gross Basis: Always compare premium quotes across SAHIs and General Insurers on a GST-inclusive (Gross Premium) basis to get an accurate picture of the total household cash outflow, especially when evaluating steep senior citizen policies.

Strategic Consolidation: Consider purchasing a higher sum insured base policy rather than relying on multiple smaller, fragmented top-ups. The GST structure and policy administration charges make consolidation more mathematically cost-efficient in many underwriting scenarios.

Financial Planning for HNIs: Banking and finance professionals advising High-Net-Worth clients must aggressively factor in the escalating GST component combined with medical inflation when structuring comprehensive, multi-decade financial plans, particularly for those approaching retirement.

The broader point stands: GST on health insurance India premiums remains one of the most consequential yet underappreciated levers in India's health financing architecture. A well-calibrated reform here could do more for insurance penetration than almost any other single policy intervention. For a country where out-of-pocket health expenditure remains stubbornly high and medical inflation consistently outpaces general inflation, getting the tax policy right on health insurance is not a marginal issue — it is a foundational one. Bankopedia will continue tracking the GST Council's deliberations and IRDAI's policy positions as this critical debate unfolds.