India's Digital Rupee (CBDC): A Complete Guide to the e-Rupee and What It Means for You

The India digital rupee CBDC explained in its simplest form: it is sovereign money, issued by the Reserve Bank of India (RBI), that exists purely in digital form. Unlike a bank balance that represents a claim on a commercial bank, the e-Rupee is a direct liability of the central bank — the digital equivalent of holding a ₹500 note in your wallet, except it lives on a device. Since the RBI formally launched pilot programmes for both the wholesale and retail variants of its Central Bank Digital Currency (CBDC) in late 2022, the conversation around digital money in India has moved decisively from academic curiosity to policy priority. With India's welfare architecture disbursing over ₹6 lakh crore annually across subsidies, pensions, and direct benefit transfers, the stakes for getting CBDC right could hardly be higher. This guide unpacks how the e-Rupee works, how it compares with UPI and cash, and why policymakers believe it could finally seal the leaks in India's vast subsidy pipeline.

What Is the Digital Rupee and How Does RBI's CBDC Work?

A Central Bank Digital Currency is a tokenised, digital form of a country's fiat currency, issued and backed by the central bank. In India's case, the RBI is the sole issuing authority under the amended Section 22 of the Reserve Bank of India Act, 1934, which was modified through the Finance Act 2022 to give the RBI explicit legal authority to issue digital currency. The e-Rupee is therefore legal tender in the same manner as a physical banknote — a ₹100 e-Rupee token is worth exactly ₹100, redeemable at face value, with no credit risk attached to it.

The Token-Based Architecture

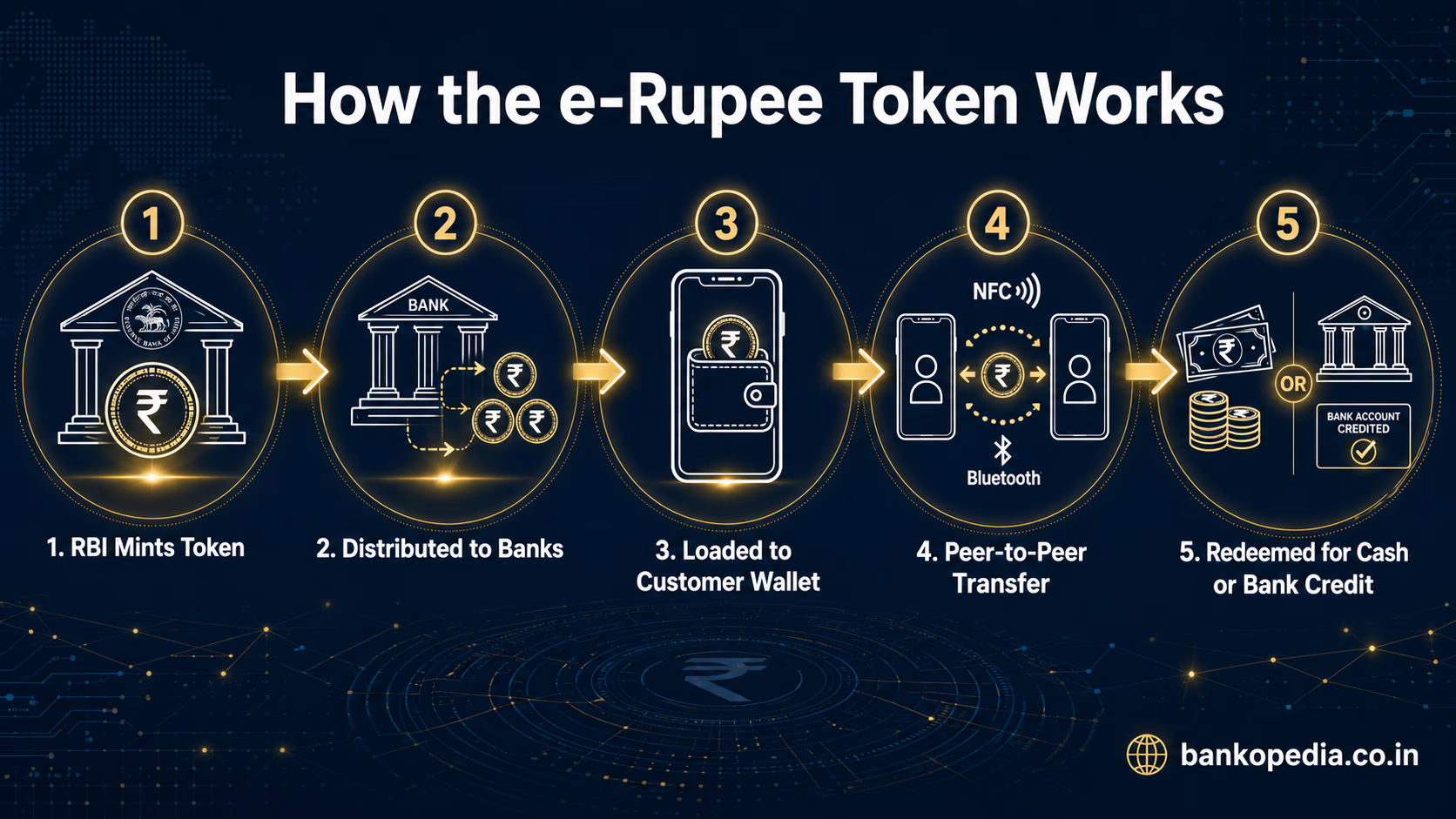

RBI's CBDC operates on a token-based model rather than an account-based one (though hybrid approaches are being explored). Here's how the chain works in practice:

The RBI mints digital tokens and distributes them to participating commercial banks — currently including SBI, HDFC Bank, ICICI Bank, Kotak Mahindra Bank, Yes Bank, IDFC First Bank, HSBC India, and Bank of Baroda, among others.

These banks load the tokens into digital wallets hosted on customers' smartphones.

A customer can transfer tokens peer-to-peer, offline or online, without the transaction necessarily touching a bank account in real time.

The receiving party holds the token, which can be redeemed at any participating bank for physical cash or credited to a bank account.

This token architecture has a critical implication: transactions can theoretically be executed without internet connectivity, using Near Field Communication (NFC) or Bluetooth-based protocols. The RBI has been actively piloting offline functionality, recognising that over 300 million Indians still have unreliable internet access — a gap that UPI and mobile banking cannot bridge as effectively.

Wholesale CBDC vs. Retail CBDC

RBI's CBDC comes in two flavours. The e₹-W (wholesale) variant, piloted first in November 2022, is restricted to financial institutions for settling interbank transactions, government securities trades, and cross-border payments. The Clearing Corporation of India Limited (CCIL), which sits at the heart of India's financial market infrastructure, has been deeply involved in testing wholesale CBDC settlement — a development directly relevant as the CCIL chief has highlighted the need for financial market infrastructure to keep pace with volatile geopolitics and shifting global payment architectures.

The e₹-R (retail) variant, launched in December 2022, is what concerns everyday Indians. It is designed to function as a digital complement to physical cash, accessible to consumers and merchants through a dedicated wallet application provided by participating banks. Crucially, the e₹-R wallet does not earn interest — it is a transactional instrument, not a savings vehicle, preserving the distinction between money and banking.

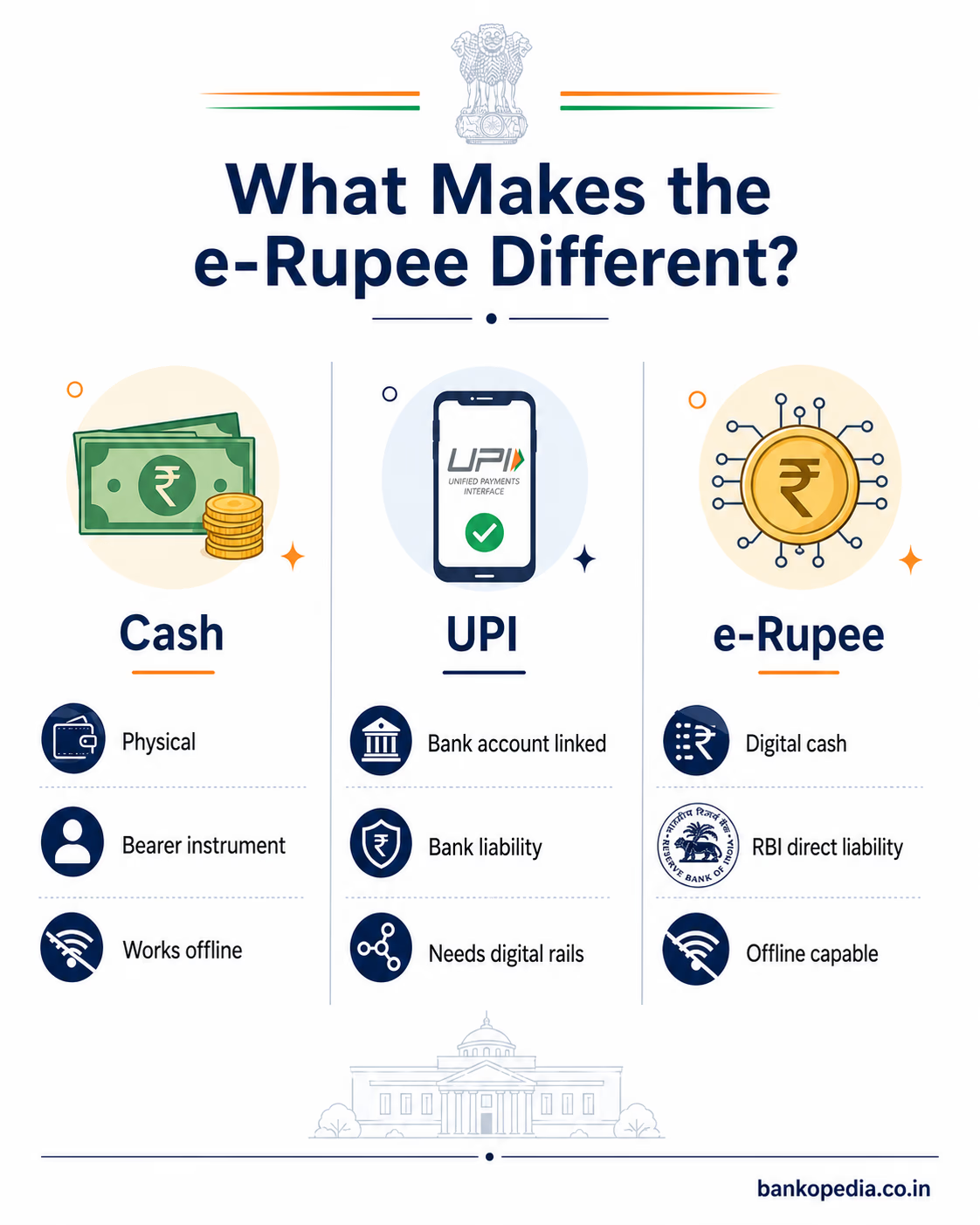

Digital Rupee vs UPI vs Cryptocurrency: Key Differences

One of the most persistent sources of confusion in public discourse is the conflation of the digital rupee with UPI or, worse, with cryptocurrencies. These are fundamentally distinct instruments, and the differences carry real consequences for users, regulators, and the financial system.

Digital Rupee vs UPI

UPI — the Unified Payments Interface governed by NPCI — is a payment rail, not a form of money. When you send ₹1,000 via PhonePe or Google Pay using UPI, you are instructing your bank to debit your account and credit the recipient's. The money that moves is a commercial bank liability. UPI is a messaging and clearing layer that sits on top of existing bank accounts.

The digital rupee, by contrast, is the money itself. Consider this table of distinctions:

Issuer: UPI moves commercial bank money; e-Rupee is issued by the RBI — a sovereign, zero-default-risk instrument.

Internet dependency: UPI requires an active internet or telecom connection; e-Rupee can work offline once tokens are loaded on a device.

Settlement finality: UPI transactions settle via RTGS/NEFT infrastructure with some latency; CBDC token transfer is instantaneous and final at the point of transfer.

Programmability: e-Rupee tokens can be embedded with smart contract conditions — for instance, a welfare transfer token that can only be spent at authorised ration shops — a capability UPI's current architecture does not natively support.

Anonymity: Cash is fully anonymous; UPI is fully traceable; CBDC is being designed with tiered privacy — low-value transactions may enjoy greater anonymity, while large transactions remain auditable by the RBI.

Digital Rupee vs Cryptocurrency

The contrast with private cryptocurrencies such as Bitcoin or Ethereum is even sharper. Cryptocurrencies are decentralised, unregulated, and not backed by any sovereign authority. Their value is determined purely by market sentiment. The e-Rupee, by contrast, is:

Centralised: Issued and controlled by the RBI; no mining, no algorithmic monetary policy.

Stable by design: One e-Rupee = one physical rupee; there is no speculative premium or volatility.

Legal tender: Merchants and individuals are legally obligated to accept it as payment.

Regulated: Falls squarely under RBI's regulatory perimeter, unlike private crypto assets which SEBI and RBI have repeatedly flagged as speculative instruments.

"CBDC is not cryptocurrency. Cryptocurrency is a private asset. CBDC is sovereign currency in digital form. The confusion between the two is something we must actively dispel." — RBI Governor (paraphrased from RBI's CBDC Concept Note, October 2022)

From a monetary policy perspective, CBDC also differs from cryptocurrency in a vital way: the RBI retains full control over money supply. Deputy Governor Poonam Gupta has emphasised that central banks must retain the instruments to look through transient inflation without allowing it to become entrenched — and CBDC, by remaining within the RBI's balance sheet, ensures that digital money does not escape the monetary policy transmission framework the way unregulated crypto assets do.

How CBDC Can Plug Leakages in India's Welfare and Subsidy System

Perhaps the most consequential application of the e-Rupee lies not in urban digital payments — where UPI has already achieved remarkable penetration — but in the deep, structural problem of welfare leakages. India's direct benefit transfer (DBT) architecture, managed through the JAM trinity (Jan Dhan accounts, Aadhaar, and Mobile), has already saved the government an estimated ₹3.48 lakh crore in leakages since 2013. Yet significant leakages persist, and CBDC offers tools that DBT alone cannot.

The Anatomy of Welfare Leakage

India's welfare disbursements span food subsidies under the National Food Security Act, PM-KISAN agricultural transfers, MGNREGS wages, LPG subsidies, scholarship programmes, and state-level schemes. Leakages occur at multiple nodes:

Ghost beneficiaries: Payments flowing to fictitious or deceased individuals.

Diversion: Funds received by genuine beneficiaries but spent in ways that violate programme intent — for instance, food subsidy cash being spent on non-nutritional items.

Intermediary capture: Middlemen and local power structures siphoning funds before they reach end beneficiaries.

Last-mile cash-out fraud: Business Correspondents (BCs) charging informal fees or refusing withdrawals in remote areas.

CBDC's Programmability as a Policy Tool

The transformative element of CBDC in this context is programmable money. A digital rupee token can be embedded with conditional logic at the point of issuance. This means:

Earmarking by category: An MGNREGS wage token could be programmed to be redeemable only at NABARD-accredited fair price shops or for agricultural inputs, preventing diversion to non-intended purposes.

Geographic fencing: Tokens can be restricted to spending within a specific district or at merchants registered under a particular welfare scheme.

Time-bound validity: Food subsidy tokens that must be redeemed within a quarter prevent hoarding and black-market resales.

Elimination of intermediaries: CBDC tokens delivered directly to a beneficiary's wallet bypass the BC layer for disbursement, removing a significant source of intermediary rent-seeking.

This is precisely the capability that NABARD and the Finance Ministry are reportedly exploring as they examine how CBDC-based agricultural credit and subsidy disbursements could replace current mechanisms. The programmability of CBDC is not merely a fintech novelty — it is a genuine instrument of fiscal governance.

Traceability Without Full Surveillance

A reasonable concern about programmable welfare money is that it could become a surveillance instrument — tracking beneficiaries' every purchase and penalising spending choices. RBI's design philosophy attempts to balance this through tiered anonymity. Small-value subsidy transactions would maintain a degree of privacy, while systemic audits can trace aggregate flows without granular personal data being exposed. This is analogous to how physical cash is private at the individual level but traceable at the systemic level through currency circulation data.

IRDAI is also paying attention: micro-insurance premiums linked to agricultural welfare schemes could eventually be bundled into programmable CBDC transfers, creating an integrated social protection architecture that is self-executing and audit-ready.Current Status and Rollout Roadmap of e-Rupee in India

As of 2026, India's CBDC programme has matured from its early experimental phases into a structurally integrated financial tool. While it has not yet dethroned UPI to achieve mass-market dominance, its foundational capabilities are solidifying. Here is where the ecosystem currently stands:

Milestones and Market Realities

Network Expansion: The retail CBDC network now spans across major cities and Tier-2 regions, supported by a robust consortium of public and private sector banks.

The Transaction Volume Context: While pilot phases famously achieved peaks of over 1 million daily transactions, it is now understood that this surge was heavily engineered by commercial banks routing employee salaries and benefits through the system to meet RBI distribution targets. Genuine, organic consumer usage remains a fraction of UPI's daily volume.

Proving the Offline Concept: The offline CBDC pilots—tested in areas with low connectivity in Tier 3 and Tier 4 cities—have successfully demonstrated secure, device-to-device transfers without internet connectivity. This is a critical milestone that directly addresses India's digital divide and sets the e-Rupee apart from existing payment rails.

Persistent Friction Points The RBI has remained candid about the hurdles of consumer adoption. UPI already satisfies most digital payment needs with a near-flawless user experience, creating significant behavioral inertia. Key friction points include:

Zero-Yield Wallets: Because CBDC wallets are designed to be purely transactional and do not earn interest (to prevent cannibalising commercial bank deposits), they lack the financial incentive of a savings account or the reward structures often attached to private UPI apps.

Wallet Fatigue: Initially, the requirement to download and fund a completely separate app created substantial user friction in an already saturated digital payments market.

Merchant Education: Training merchants, particularly in semi-urban and rural geographies, to understand the backend distinction between sovereign digital money and standard commercial bank transfers remains a resource-intensive challenge.

The Strategic Horizon Moving forward, the RBI's focus has shifted from mere issuance to deep structural integration and targeted use cases:

UPI Interoperability (The Lifeline): Once a "road ahead" objective, the integration with UPI infrastructure is now a functional reality. Users can seamlessly scan existing UPI QR codes and pay via their e-Rupee wallets. This interoperability has dramatically reduced friction and is currently the primary driver keeping the retail CBDC relevant in everyday commerce.

Executing Programmable Welfare: The theoretical promise of programmable money is moving into practical application. The RBI, in partnership with the Ministry of Finance and NABARD, is actively transitioning toward live pilots of conditional CBDC transfers for state-level agricultural and social welfare schemes.

Cross-Border Corridors: India is aggressively positioning the e-Rupee as a tool for international trade and remittances. Through engagement with BIS-led initiatives like Project Nexus and bilateral corridor discussions with SAARC and Gulf nations, the ultimate goal is to use wholesale and retail CBDC to bypass slow, expensive correspondent banking networks.

Private Sector Layering: Similar to how third-party applications (like PhonePe or Google Pay) built the user experience on top of the NPCI's UPI rail, the RBI aims to allow regulated fintech companies to build innovative, value-added services directly on top of the sovereign CBDC layer.

Conclusion: What the e-Rupee Means for Everyday Indians

The digital rupee is not a replacement for UPI, nor is it a response to cryptocurrency hype. It is a carefully considered addition to India's monetary architecture — one that combines the trust and finality of physical cash with the programmability and traceability of digital systems. For the urban professional, the immediate impact may feel minimal: UPI works perfectly well, and the e-Rupee offers few compelling advantages in daily life right now. But for the agricultural labourer in Chhattisgarh receiving MGNREGS wages, the widow in Rajasthan entitled to a pension that currently passes through three intermediaries, or the farmer in Vidarbha waiting for a PM-KISAN instalment, the programmable, directly-delivered, offline-capable digital rupee could represent a genuine improvement in financial access and benefit delivery.

The RBI's approach has been deliberately measured — learning from China's aggressive e-CNY rollout while avoiding the coercive adoption mandates that have drawn criticism elsewhere. As CBDC infrastructure matures, its integration with India's DBT architecture, NABARD-linked agricultural credit pipelines, and eventually cross-border payment corridors will determine whether the e-Rupee becomes a transformational policy instrument or remains a well-designed solution in search of scale.

For banking professionals, the message is clear: CBDC is not a distant experiment. It is live, it is expanding, and understanding its architecture, its regulatory foundations, and its policy applications is no longer optional for anyone serious about India's evolving financial landscape.